[This is a large excerpt from an excellent 18-page paper I think predicts how the future will unfold as well as a good overview of our predicament. Alice Friedemann]

Fantazzini, Dean; Höök, Mikael; Angelantoni, André. 2011. Global oil risks in the early 21st century. Energy Policy, Vol. 39, Issue 12: 7865-7873

http://dx.doi.org/10.1016/j.enpol.2011.09.035

The Deepwater Horizon incident demonstrated that most of the oil left is deep offshore or in other difficult to reach locations. Moreover, obtaining the oil remaining in currently producing reservoirs requires additional equipment and technology that comes at a higher price in both capital and energy. In this regard, the physical limitations on producing ever-increasing quantities of oil are highlighted as well as the possibility of the peak of production occurring this decade. The economics of oil supply and demand are also briefly discussed showing why the available supply is basically fixed in the short to medium term. Also, an alarm bell for economic recessions is shown to be when energy takes a disproportionate amount of total consumer expenditures. In this context, risk mitigation practices in government and business are called for. As for the former, early education of the citizenry of the risk of economic contraction is a prudent policy to minimize potential future social discord. As for the latter, all business operations should be examined with the aim of building in resilience and preparing for a scenario in which capital and energy are much more expensive than in the business-as-usual one.

An economy needs energy to produce goods and deliver services and the size of an economy is highly correlated with how much energy it uses (Brown et al., 2010a, Warr and Ayers, 2010). Oil has been a key element of the growing economy. Since 1845, oil production has increased from virtually nothing to approximately 86 million barrels per day (Mb/d) today (IEA, 2010), which has permitted living standards to increase around the world. In 2004 oil production growth stopped while energy hungry and growing countries like China and India continued increasing their demand. A global price spike was the result, which was closely followed by a price crash. Since 2004 world oil production has remained within 5% of its peak despite historically high prices (see Figure 1).

The combination of increasingly difficult-to-extract conventional oil combined with depleting super-giant and giant oil fields, some of which have been producing for 7 decades, has led the International Energy Agency (IEA) to declare in late 2010 that the peak of conventional oil production occurred in 2006 (IEA, 2010). Conventional crude oil makes up the largest share of all liquids commonly counted as “oil” and refers to reservoirs that primarily allow oil to be recovered as a free-flowing dark to light-colored liquid (Speight, 2007). The peak of conventional oil production is an important turning point for the world energy system because many difficult questions remain unanswered. For instance: how long will conventional oil production stay on its current production plateau? Can unconventional oil production make up for the decline of conventional oil? What are the consequences to the world economy when overall oil production declines, as it eventually must? What are the steps businesses and governments can take now to prepare? In this paper we pay particular attention to oil for several reasons. First, most alternative energy sources are not replacements for oil. Many of these alternatives (wind, solar, geothermal, etc.) produce electricity— not liquid fuel. Consequently the world transportation fleet is at high risk of suffering from oil price shocks and oil shortages as conventional oil production declines. Though substitute liquid fuel production, like coal-to-liquids, will increase over the next two or three decades, it is not clear that it can completely make up for the decline of oil production. Second, oil contributes the largest share to the total primary energy supply, approximately 34%. Changes to its price and availability will have worldwide impact especially because alternative sources currently contribute so little to the world energy system (IEA, 2010).

Oil is particularly important because of its unique role in the global energy system and the global economy. Oil supplies over 90% of the energy for world transportation (Sorrell et al., 2009). Its energy density and portability have allowed many other systems, from mineral extraction to deep-sea fishing (two sectors particularly dependent on diesel fuel but sectors by no means unique in their dependence on oil), to operate on a global scale. Oil is also the lynchpin of the remainder of the energy system. Without it, mining coal and uranium, drilling for natural gas and even manufacturing and distributing alternative energy systems like solar panels would be significantly more difficult and expensive. Thus, oil could be considered an “enabling” resource.

Oil enables us to obtain all the other resources required to run our modern civilization.

Peak oil is the result of a complex set of forces that includes geology, reservoir physics, economics, government policies and politics.

There are a number of physical depletion mechanisms that affect oil production (Satter et al., 2008). Depletion-driven decline occurs during the primary recovery phase when decreasing reservoir pressure leads to reduced flow rates. Investment in water injection, the secondary recovery phase, can maintain or increase pressure but eventually increasingly more water and less oil is recovered over time (i.e. increasing water cut). Additional equipment and technology can be used to enhance oil recovery in the tertiary recovery phase but it comes at a higher price in terms of both invested capital and energy to maintain production.

The situation is similar to squeezing water out of a soaked sponge. It is easy at first but increasingly more effort is required for diminishing returns. At some point, it is no longer worth squeezing either the sponge or the oil basin and production is abandoned.

Another way to explain peaking oil production is in terms of predator-prey behavior, as Bardi and Lavacchi (2009) have done. Their idea is that, initially, the extraction of “easy oil” leads to increasing profit and investments in further extraction capacity. Gradually the easiest (and typically the largest) resources are depleted. Extraction costs in both energy and monetary terms rise as production moves to lower quality deposits. Eventually, investments cannot keep pace with these rising costs, declining production from mature fields cannot be overcome and total production begins to fall.

Hubbert (1982) wrote: There is a different and more fundamental cost that is independent of the monetary price. That is the energy cost of exploration and production. So long as oil is used as a source of energy, when the energy cost of recovering a barrel of oil becomes greater than the energy content of the oil, production will cease no matter what the monetary price may be.

Currently, around 60 countries have passed “peak oil” (Sorrell et al., 2009)— their point of maximum production. In most cases this is due to physical depletion of the available resources (e.g. USA, the UK, Norway, etc.) while in a few cases socioeconomic factors limit production (e.g. Iraq).

Attempts to disprove peak oil that focus solely on the amount of oil available in all its forms demonstrate a fundamental, and unfortunately common, confusion between how much oil remains versus how quickly it can be produced. Although until recently oil appears to be more economically available than ever before (Watkins, 2006), others have shown this to be an artifact of statistical reporting (Bentley et al., 2007). Further, it is far less important how much oil is left if demand is, for instance, 90 Mb/d but only 80 Mb/d can be produced. Still, the most realistic reserve estimates indicate a near-term resource-limited production peak (Meng and Bentley, 2008; Owen et al., 2010).

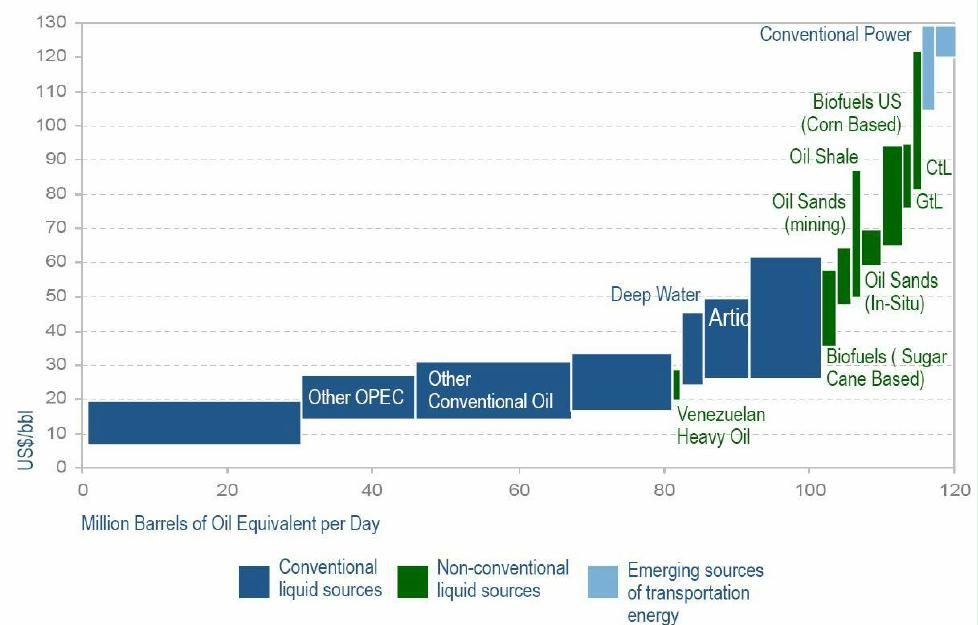

Total oil production is comprised of conventional oil, which is liquid crude that is easy and relatively cheap to pump, and unconventional oil, which is expensive and often difficult to produce. It is vital to understand that new oil is increasingly coming from unconventional sources like polar, deep water and tar sands. Almost all the oil left to us is in politically dangerous or remote regions, is trapped in challenging geology or is not even in liquid form.

Today, over 60% of the world production originates from a few hundred giant fields. The number of giant oil field discoveries peaked in the early 60s and has been dwindling since then (Höök et al., 2009). This is similar to picking strawberries in a field. We picked the biggest and best strawberries first (just like big oil fields they are easier to find) and left the small ones for later. Only 25 fields account for one quarter of global production and 100 fields account for half of production. Just 500 fields account for two-thirds of all the production (Sorrell et al., 2009).

As the IEA (2008) points out, it is far from certain that the oil industry will be able to muster the capital to tap enough of the remaining, low-return fields fast enough to make up for the decline in production from current fields.

Oil sources are not equally easy to exploit. It takes far less energy to pump oil from a reservoir still under natural pressure than to recover the bitumen from tar sands and convert it to synthetic crude. The energy obtained from an extraction process divided by the energy expended during the process is the Energy Return on Energy Invested (EROEI).

Since giant and super giant oil fields dominate current production, they are good indicators for the point of peak production (Robelius, 2007; Höök et al., 2009). There is now broad agreement among analysts that the decline in existing production is between 4-8% annually (Höök et al., 2009). In terms of capacity, this means that roughly a new North Sea (~5 Mb/d) has to come on stream every year just to keep the present output constant.

Peak oil is the point in time where production flows are unable to increase. It is not just underinvestment, political gamesmanship or remote locations that make oil production increasingly difficult. The physical depletion mechanisms (increasing water cut, falling reservoir pressure, etc.) will unavoidably affect production by imposing restrictions and even limitations on the future production of liquid crude oil. No amount of technology or capital can overcome this fact.

Some consequences of having extracted much of the easy oil are the following:

- It takes significantly more time once a field is discovered to start production. Maugeri (2010) estimates it now takes between 8 and 12 years for new projects to produce first oil. Difficult development conditions can delay the start of production considerably. In the case of Kashagan, the world’s largest oil discovery in 30 years, production has been delayed by almost ten years due to difficult environmental conditions.

- In mature regions, an increased drilling effort usually results in little increase in oil production because the largest fields were found and produced first (Höök and Aleklett, 2008; Höök et al., 2009).

- Because the cost of extracting the remaining oil is much higher than easy-to-extract OPEC or other conventional oil, if the market price remains lower than the marginal cost for long enough producers will cut production to avoid financial losses. See Figure 3.

- Uncertainty about future economic growth heightens concerns for executing these riskier projects. This delays or often cancels projects (Figure 4).

- Most remaining oil reserves are in the hands of governments. They tend to under-invest compared to private companies (Deutsche Bank, 2009).

- Possible scarcity rents have to be taken into account. Hotelling (1931) showed that in the case of a depletable resource, price should exceed marginal cost even if the oil market were perfectly competitive (the resulting difference is called scarcity rent).

If this were not the case, it would be more profitable to leave the oil in the ground, waiting to produce it until the price has risen. Hamilton (2009a, 2009b) noted that while in the 1990s the scarcity rent was negligible relative to costs of extraction, the strong demand growth from developing countries in the last decade together with limits to expanding production could in principle account for a sudden shift to a regime in which the scarcity rent is positive and quite important. In this regard, the Reuters news service reported on April 13, 2008 that Saudi Arabia’s King Abdullah said he had ordered some new oil discoveries left untapped to preserve oil wealth in the world’s top exporter for future generations, the official Saudi Press Agency (SPA) reported. Therefore, a possible intertemporal calculation considering scarcity rents may have already influenced (i.e. limited) current production. Although the sudden fall of prices at the end of 2008 is difficult to reconcile with scarcity rents, the following quick price recovery to the 70$-120$ range during the enduring global financial crisis indicates that this aspect cannot be dismissed. This is despite the assertion by Reynolds and Baek (2011) that the Hotelling principle “… is not a powerful determinant of nonrenewable resources prices,” and that “…the Hubbert curve and the theory surrounding the Hubbert curve is an important determinant of oil prices.” We agree that the Hubbert curve, which defines the depletion curve of a non-renewable resource, may be the prime determinant of oil price but it is not the only one.

Figure 3. Global marginal cost of production 2008. Source: LCM Research based on Booz Allen/IEA data (Morse, 2009).

After 2014, it appears that global oil production will begin its decline (See the second report of the UK Industry Taskforce on Peak Oil and Energy Security (UK ITPOES, 2010), Lloyd’s (2010), Deutsche Bank (2009, 2010), the report by the UK Energy Research Centre (Sorrell et al., 2009a) and the 2010 World Energy Outlook by the IEA (2010).)

Deutsche Bank (2009) asserts that for American consumers this point is when energy represents 7.5% of gross domestic product. This value is close to the one calculated by Hamilton (2009b) but is based on monthly data and uses a different methodology. In a more recent report, Deutsche Bank (2010) lowered this threshold to 6.5% because “…the last shock set in motion major behavioral and policy changes that will facilitate rapid behavioral changes when the next one comes and underemployment and weak wage growth has increased sensitivity to gasoline prices. Last time it took $4.50/gal gasoline to finally tip demand, this time it might only take $3.75/gal to $4.00/gal to do it.” However, they also highlighted that “Americans have become comfortable with paying more for gasoline, and it may take higher prices to force behavior change”.

Hamilton (2011) highlighted that 11 of the 12 U.S. Recessions since World War II were preceded by an increase in oil prices. Unfortunately, there is no clear alternative source of energy able to fully substitute for oil (see, for example, Maugeri (2010) for a recent nontechnical review of the limits of alternative sources of energy with respect to oil). It possesses a combination of energy density, portability and historically very high EROEI that is difficult for alternatives to match. 4. A timely energy system transformation not assured. As oil production declines, significant changes to the currently oil-dependent economy in the medium term are likely to be needed. However, it isn’t clear that there will the financial means to implement such a change. For example, Deutsche Bank (2009, 2010) suggested that the widespread use of electric cars in the second part of this decade will be the disruptive technology that will finally destroy oil demand. Apart from technology and resource constraints (lithium necessary for electrical batteries is quite abundant in nature but production is currently very limited), the availability of sufficient financial resources to transition the entire vehicle fleet seems dubious. As Hamilton (2009b) demonstrates, tightened credit follows high oil prices and most vehicles are purchased on credit. Others suggest that natural gas is the next energy paradigm. Again, will be there sufficient financial resources to switch to it as oil production declines? Reinhart and Rogoff (2009, 2010) found that historically, after a banking crisis, the government debt on average almost doubles (86% increase) to bail out the banks and to stimulate the economy. They also showed that a sovereign debt crisis usually follows, not surprisingly as we saw Iceland, Greece, Ireland, Hungary and Portugal turning to the EU/ECB and/or the IMF for financial help to refinance their public debts to avoid default. The need to switch to alternative energy sources with the enormous financial investments that such a task would require— and the simultaneous presence of large public and private debts — may well form a perfect storm.

Demography will also be extremely important in the next decade as well. Europe and the United States have aging populations and their baby boomers are entering pension age. China faces a similar demographic problem due to their one child policy, too.

The combination of declining oil production (and thus oil priced high enough to cause recessions), high taxes, austerity measures, more restrictive credit conditions and demographic shifts have the potential to severely constrain the financial resources needed to move the economy away from oil and to alternative energy sources. Another consequence of this combination of forces is the likely contraction of the world economy (Hamilton, 2009b; Dargay and Gately, 2010).

Businesses and governments struggle with alternating circumstances of insufficient cash flow to handle price spikes and plummeting prices that don’t cover their cost structure. Long term planning in this ever-changing environment becomes extremely difficult and investment — even highly needed investment — can drop precipitously.

Friedrichs (2010) also cautions that after peak oil countries have several sociological trajectories available to them: they can follow predatory militarism like Japan before WWII, totalitarian retrenchment like North Korea, or, ideally, socioeconomic adaptation like Cuba after the fall of the Soviet Union. Given the recent century of conflict and the extensive weapon stocks and militaries held by modern nations (especially the United States, which spends on its military almost as much as the remaining countries of the world combined (SIPRI, 2011), there is simply no guarantee that the relatively peaceful period currently experienced by developed nations that is conducive to rapid energy source transitions will continue much longer.

A further challenge is that, strictly speaking, for the last 150 years we have not transitioned from previous fuel sources to new ones — we have been adding them to the total supply. We are currently using all significant sources (coal, oil, gas and uranium) at high rates. Thus, it’s common but incorrect to say that we moved from coal to oil. In fact, we are using more coal now than we ever have (IEA, 2010). We never left the coal age. The challenge of moving to alternative energy sources while a particularly important source is declining, in this case oil, should not be underestimated.

Brown et al. (2010b) show how significant the squeeze of declining gross production and increasing producer country consumption can be, which they have named the Export Land Model. Increasing producer country consumption due to population growth acts as a strong magnification factor that removes oil very quickly from the export market. Using the top five exporting countries from 2005 (Saudi Arabia, Russia, Norway, Iran and United Arab Emirates), they construct a scenario in which combined production declines at a very slight 0.5% per year over a ten year period for a total of 5%. Internal oil consumption for these exporters continues to grow at its current rate (2010). In this scenario net oil exports decline by 9.6%, almost double the rate oil production declines.

This accelerated loss of exportable oil can be seen in many producer countries that have passed their peak. Indonesia has withdrawn from OPEC because they have no more exportable oil to offer the world market. Egypt is already incurring a public debt and is on the cusp of becoming a net oil importer, which will exacerbate already stretched public finances. As producer countries continue to grow their oil use even modestly and production declines (again, even modestly), there is an extremely high risk that net exportable oil will decline much faster than most observers are currently expecting.

Other mitigation efforts like increased solar, wind and geothermal production may not be prioritized since they do not help the situation — they produce electricity and the world’s 800 million transportation, food production (i.e. tractors and harvesters) and distribution vehicles require liquid fuel.

A contracting economy presents governments with a host of problems that are not easy to resolve. Promises made to the citizenry, some in the form of social welfare programs, pensions and public union contracts, will be impossible to keep as the energy base of the economy declines. Downward wage pressure and reduced business activity will lower tax revenue. With lower revenues and greater demands in the form of social welfare support by an increasingly poorer citizenry, it is difficult to see how the accumulated (and growing) government debt can be paid back without rampant inflation. Though it is still unclear whether the government response will be hyperinflation (to minimize the debts) or extensive and massive debt defaults (deflation) — or both — it is not likely that business as usual will continue as oil production declines.

Some governments may also have to contend with food and fuel riots as they did in 2007 and 2008. Other forms of crowd behavior, namely hoarding of fuel and food, may exacerbate the situation and governments should prepare accordingly.

Supply Chains

Manufacturers in particular will have to contend with increased difficulties making and delivering products as oil production declines (Hirsch et al., 2005). It will prove imperative that business addresses this Schumpetarian shock (a structural change to industry that can alter what is strategically relevant) in a timely fashion (Barney, 1991). A significant benefit of cheap oil was that distance was relatively inexpensive. It is possible now to manufacture goods using far-flung operations. However, as oil declines, distance will, once again, become increasingly expensive, and oil price may begin to act as a trade barrier for many products. Another risk as oil production declines is the possibility of oil supply disruptions. If this should occur, much modern manufacturing may be impacted. Just-in-time manufacturing systems in which warehoused parts are minimized through the frequent replenishment of parts by parts suppliers — sometimes with multiple deliveries a day— have little tolerance for delivery delays. To prepare for this risk requires more than the drive for manufacturing efficiency that has generally characterized business. Supply chains should be examined with the aim of building in resilience and greater agility (Bunce and Gould, 1996; Krishnamurthy 2007), implying the loosening of tight and often brittle couplings between suppliers and manufacturers (Christopher 2000; Towill 2001, Mitch Leppo ). With little or no slack in the system (fewer warehoused parts, etc.), just one supplier failing to deliver a part or supplier hoarding can shut down a production process.

References

Adelman, M.A., 1990. Mineral depletion, with special reference to petroleum. Review of Economics and Statistics, 72(1), 1–10.

Aleklett, K., Höök, M., Jakobsson, K., Lardelli, M., Snowden, S., Söderbergh, B., 2010. The Peak of the Oil Age — analyzing the world oil production Reference Scenario in World Energy Outlook 2008. Energy Policy, 38(3), 1398-1414.

Bardi, U., 2007. Energy Prices and Resource Depletion: Lessons from the Case of Whaling in the Nineteenth Century. Energy Sources, Part B: Economics, Planning, and Policy, 2(3), 297–304.

Bardi, U., Lavacchi, A., 2009. A simple interpretation of Hubbert‟s model of resource exploitation. Energies 2(3), 646–661.

Barney, J.B. 1991. Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99-120.

BCBS Consultative Proposal, 2009. Strengthening the resilience of the banking sector. Available from: http://www.bis.org/publ/bcbs164.htm

Belzowski, B.M., McManus, W., 2010. Alternative power train strategies and fleet turnover in the 21st century. University of Michigan, report no. UMTRI-2010-20, August 2010.

Bentley, R.W., Mannan, S.A., Wheeler, S.J., 2007. Assessing the date of the global oil peak: the need to use 2P reserves. Energy Policy 35(12), 6364–6382.

BP, 2010. BP Statistical Review of World Energy 2010. See also: http://www.bp.com

Brown, J.H., Burnside, W.R., Davidsson, A.D., DeLong, J.P., Dunn, W.C., Hamilton, M.J., Mercado-Silva, N., Nekola, J.C., Okie, J.G., Woodruff, W.H., Zuo, W. 2010a. Energetic limits to economic growth. Bioscience, 61(1), 19-26.

Brown, J., Foucher, S., Silveus, J., 2010b. Peak Oil Versus Peak Net Exports — Which Should We Be More Concerned About? Association for the Study of Peak Oil and Gas presentation in Washington D.C., 8 October 2010, http://aspousa.org/2010presentationfiles/10-7-2010_aspousa_TrackBNetExports_Brown_J.pdf

Bunce, P., Gould, P., 1996. From Lean to Agile Manufacturing. IEE Colloquium Digest, 1996, Issue 278.

Cameron, K., and Schnusenberg, O., 2009. Oil prices, SUVs, and Iraq: An investigation of automobile manufacturer oil price sensitivity. Energy Economics, 31(3), 375-381.

Campbell, C.J., 1997. The coming oil crisis. Multi-Science Publishing, Brentwood.

Campbell, C.J., 2002. Petroleum and people. Population & Environment, 24(2), 193–207.

CIA Factbook, 2010. The World Factbook. See also: https://www.cia.gov/library/publications/the-world-factbook/

Christopher, M., Towill, D.R., 2000. Marrying the Lean and Agile Paradigms. Proc. EUROMA Conference, Ghent, 2000, 114-121.

Dargay J.M., Gately, D., 2010. World oil demand‟s shifttoward faster growing and less price-responsive products and regions. Energy Policy, 38(10), 6261-6277.

Deutsche Bank, 2009. The Peak Oil Market — price dynamics at the end of the oil age. Deutsche Bank Securities.

Deutsche Bank, 2010. The End of the Oil Age. 2011 and beyond: A reality check. Global Markets Research.

Friedrichs, J., 2010. Global energy crunch: How different parts of the world would react to a peak oil scenario. Energy Policy, 38(8), 4562–4569.

Gately, M., 2007. The EROI of U.S. offshore energy extraction: A net energy analysis of the Gulf of Mexico. Ecological Economics, 63(2-3), 355-364.

Hall, C.A.S., Powers, R., Schoenberg, W., 2008. Peak Oil, EROI, investments and the economy in an uncertain future. In: Pimentel, D (Ed.) Biofuels, solar and wind as renewable energy systems. Springer, New York.

Hall C.A.S., Balogh, S., Murphy, D.J.R., 2009. What is the Minimum EROI that a Sustainable Society Must Have? Energies, 2(1), 25-47. http://dx.doi.org/10.3390/en20100025

Hamilton, J., 2009a. Understanding crude oil prices, Energy Journal, 30(2), 179-206.

Hamilton, J., 2009b. Causes and consequences of the oil shock of 2007-08. Brookings Papers on Economic Activity, Spring 2009, 215-259.

Hamilton, J., 2011. Historical oil shocks. In: Parker, R.E., Whaples, R.M. (Ed.), Handbook of Major Events in Economic History, Routledge, ISBN: 978-0415677035

Hirsch, R.L., Bezdec, R., Wendling, R., 2005. Peaking of world oil production: impacts, mitigation, & risk management. See also: http://www.netl.doe.gov/publications/others/pdf/Oil_Peaking_NETL.pdf

Hirsch, R., 2008. Mitigation of maximum world oil production: Shortage scenarios. Energy Policy, 36(2), 881–889.

Hirsch, R., 2010. The impending world energy mess. Association for the Study of Peak Oil and Gas presentation in Washington D.C., 8 October 2010, http://www.aspousa.org/2010presentationfiles/10-8-2010_aspousa_KeynoteEnergyMess_Hirsch_R.pdf

Höök, M., Aleklett, K., 2008. A decline rate study of Norwegian oil production. Energy Policy, 36(11), 4262-4271.

Höök, M., Bardi, U., Feng, L., Pang, X., 2010. Development of oil formation theories and their importance for peak oil. Marine and Petroleum Geology, 27(9), 1995-2004.

Höök, M., Hirsch, R., Aleklett, K., 2009. Giant oil field decline rates and their influence on world oil production. Energy Policy, 37(6), 2262-2272.

Hotelling, H., 1931. The economics of exhaustible resources. Journal of Political Economy, 39, 137-175.

Hubbert, M.K., 1949. Energy from fossil fuels. Science, 109(2823), 103–109.

Hubbert MK, 1956. Nuclear energy and the fossil fuels. Presented before the Spring Meeting of the Southern District, American Petroleum Institute, Plaza Hotel, San Antonio, Texas, March 7–9, http://www.hubbertpeak.com/Hubbert/1956/1956.pdf

Hubbert, M.K., 1982. Response to David Nissen http://www.hubbertpeak.com/Hubbert/to_nissen.htm

International Energy Agency, 2007. World Energy Outlook 2007. See also: http://www.worldenergyoutlook.org/

International Energy Agency, 2010. World Energy Outlook 2010. See also: http://www.worldenergyoutlook.org/

Kilian, L., 2008. Exogenous oil supply shocks: how big are they and how much do they matter for the U.S. economy? Review of Economics and Statistics, 90(2), 216-240.

Kilian, L., 2009. Not all oil price shocks are alike: disentangling demand and supply shocks in the crude oil market. American Economic Review, 99(3), 1053-1069.

Krishnamurthy, R. and Yauch, C.A. 2007. Leagile manufacturing: a proposed corporate infrastructure. International Journal of Operations & Production Management, 27(6), 588–604.

Koetse, M., de Groot, H., Florax, R. 2008. Capital-energy substitution and shifts in factor demand: A meta-analysis. Energy Economics, 30, 2236–2251.

Kopits, S., 2009. Oil: What price can America afford? Douglas Westwood Energy Business Analysts, Research Note, June 2009

Lloyd’s of London and Chatham House, 2010. Sustainable energy security — strategic risks and opportunities for business. Lloyd’s of London white paper on sustainable energy security. See also: http://www.lloyds.com/~/media/Lloyds/Reports/360%20Energy%20Security/7238_Lloyds_360_Energy_Pages.pdf

Lynch, M.C., 2002. Forecasting oil supply: theory and practice. The Quarterly Review of Economics and Finance, 42(2), 373–389.

Lynch, M.C., 2003. The new pessimism about petroleum resources: debunking the Hubbert model (and Hubbert modelers). Minerals & Energy – Raw Materials Report, 18(1), 21–32.

Maugeri, L., 2010. Beyond the age of oil. Praeger, New York.

Meng, Q.Y., Bentley, R.W., 2008. Global oil peaking: responding to the case for „abundant supplies of oil. Energy, 33(8), 1179-1184.

Miller, R.G., 2011. Future oil supply: the changing stance of the International Energy Agency. Energy Policy, 39(3), 1569–1574.

Morse, E., 2009. New oil market realities. National Association of State Energy officials conference presentation in Washington, D.C. 2009, LCM Research using Booz Allen, IEA data https://www.naseo.org/events/summer/2009/Ed%20Morse.pdf

Murphy, D.J., Hall, C.A.S., 2010. Year in review — EROI or energy return on (energy) invested. Annals of the New York Academy of Sciences, 1185, 102–118.

Owen, N.A., Inderwildi, O.R., King, D.A., 2010. The status of conventional world oil reserves — Hype or cause for concern? Energy Policy, 38(8), 4743-4749.

Reinhart, C., Rogoff, K., 2009. This time is different: eight centuries of financial folly. Princeton University Press, New Jersey.

Reinhart, C. Rogoff, K., 2010. After the fall. Federal Reserve Bank of Kansas City economic policy symposium ―Macroeconomic Policy: Post-Crisis and Risks Ahead‖ held at Jackson Hole, Wyoming, on August 26-28, 2010.

Reynolds, D.B., Baek, J., 2011. Much ado about Hotelling: Beware the ides of Hubbert, Energy Economics, article in press

Robelius, F., 2007. Giant oil fields — the highway to oil: giant oil fields and their importance for future oil production. Doctoral thesis, from Uppsala University, http://uu.diva-portal.org/smash/record.jsf?pid=diva2:169774

Rubin, J., Buchanan, P., 2007. OPEC‟s growing call on itself. CIBC Worldmarkets. http://research.cibcwm.com/economic_public/download/occrept62.pdf

Satter, A., Iqbal, G.M., Buchwalter, J.L., 2008. Practical Enhanced Reservoir Engineering. Pennwell Books. Tulsa.

Speight, J., 2008. Synthetic Fuels Handbook: Properties, Process, and Performance. McGraw-Hill Professional,

Sorrell, S., Speirs, J., Bentley R., Brandt A., Miller, R., 2009a. An assessment of the evidence for a near-term peak in global oil production, UK Energy Research Centre, London.

Sorrell, S., Speirs, J., Bentley, R. Brandt, A., Miller, R., 2009b. Global oil depletion: A review of the evidence. Energy Policy, 38(9), 5290-5295.

Towill, D.R., Christopher, M., 2001. The supply chain strategy conundrum ~ to be Lean or Agile or to be Lean and Agile. Proceedings of the International Logistics Symposium, Salzburg, 2001, pp 3-12.

UK Industry Task Force on Peak Oil and Energy Security, 2010. The Oil Crunch — a wake-up call for the UK economy. Second report of the UK ITPOES.

Warr, B.S., Ayres, R.U., 2010. Evidence of causality between the quantity and quality of energy consumption and economic growth. Energy, 35(4), 1688–1693.

Watkins, G.C., 2006. Oil scarcity: what have the past three decades revealed? Energy Policy 34(5), 508–514.

Wei, Y., Wang, Y. and Huang, D., 2010. Forecasting crude oil market volatility: Further evidence using GARCH-class models. Energy Economics, 32(6), 1477-1484.

World Bank, 2001. Finance for growth: policy choices in a volatile world – a World Bank Policy Research Report. Washington D.C.: World Bank.