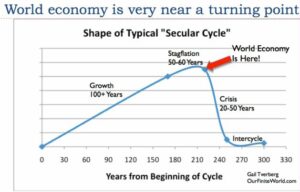

Source: Chart made by Gail Tverberg here showing the general pattern of secular cycles based on information given in the book Secular Cycles by Peter Turchin & Sergey Nefedov, Princeton University Press, 2009.

Preface. I have no idea who wrote post, Ya tenemos fecha para el cenit de la civilización. mayo 23, 2024 at https://futurocienciaficcionymatrix.blogspot.com/

This is the English translation from google. The rough peaking date for civilization is around 2025-2026 given: 1) peak oil soon , but still on a plateau until the Permian fracked oil peaks (likely 2) same for peak copper in 2025-6 (essential for all renewable contraptions to replace oil, vehicles, batteries etc), and 3) at some point (date not specified here) the tremendous debt-supply bubble will burst. If the images from the article have vanished, go to the original article to see them.

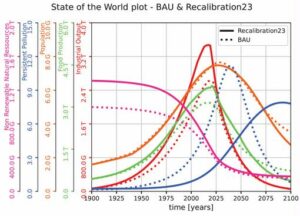

Also, the latest Limits to Growth projection:  Source: Nebel A et al (2023) Recalibration of limits to growth: An update of the World3 model. Journal of Industrial Ecology. This improved parameter set results in a World3 simulation that shows the same overshoot and collapse mode in the coming decade as the original business as usual scenario of the 1972 LtG standard run.

Source: Nebel A et al (2023) Recalibration of limits to growth: An update of the World3 model. Journal of Industrial Ecology. This improved parameter set results in a World3 simulation that shows the same overshoot and collapse mode in the coming decade as the original business as usual scenario of the 1972 LtG standard run.

Ya tenemos fecha para el cenit de la civilización

Defending the thesis of the zenith of civilization is complex, in the midst of a bubble of everything. Supporters of infinite growth often allude to improving quality of life, high-maximum bags, full bars and overflowing tourism, as an obvious justification for an opulent and growing society, at least in the West.

When a substantial change is predicted, due to the depletion of resources accompanied by virtually unpayable global debt (which is perpetuated with new debt issues to settle interest rates and finance the growing budget deficits), the first question arises immediately, on when this zenith will occur.

It is not enough to say that it is a process that takes place over tens of years, it is essential to advance a date, to “check” the reliability of the thesis.

So far, the date was more marked by the arrival of the peak oil in November 2018, but as we continue on a production plateau, around 82 million b/d, until that plateau becomes a significant decrease, we will not be able to take the beginning of the decline valid.

[My note: it looks like crude oil production will be slightly higher in 2025 than in 2018]

Since everyone has a plan, the zenith has always been questioned by human ingenuity. The rare skill of our species, which manages to find miraculous solutions to any glimpse of falling growth, has led to the creation of an alternative plan. The so-called energy transition will solve all our problems all of our problems at once. Not only will it solve climate change, but it will also send oil (and fossil fuels) to the “hell” from which they should never have left and will finally achieve, eliminate our total dependence on the viscous and black element.

But if society has grown for seventy years thanks to oil, the transition means total electrification, with copper as a vital element that intervenes in all sectors leading the energy transition. It is essential in the construction of network infrastructures, in the generation of wind and photovoltaic energy, in the implementation of electric mobility, in the extended application of a backup battery system and in general, in all processes in which electricity intervenes.

Exhausting vital resources.

So far we had a roadmap that marks the years 2025-2026, as the beginning of the decline in oil production in the American shale oil (responsible almost alone for the increase in oil production in the last decade). Conventional production peaked in 2005 and remained on a plateau until 2016-2017. The unconventional oil of shale oil, helped reach a new peak and since then, we are waiting for the descent for the unconventional, which will also mark the exit of the long plateau.

Again, this graphic is perfect for displaying both the conventional line (in red), and the sum of all oils (blue line). It can be seen as the arrival of the conventional peak, caused oil prices to enter a roller coaster, after decades of stability around $25/barrel.

It didn’t seem to matter much if oil production started to decline because we had the energy transition as a substitute. But this week the IEA (International Energy Agency) has “left” a report that warns in its base scenario (contains the projects under way plus those already approved – announced) that copper production will begin to decline in 2026, with a fundamental graph.

Therefore we have just closed the circle, putting the spotlight in 2026, when the two toughest forecasts coincide, to show the beginning of the decline in oil production and at the same time, the beginning of the fall in copper production.

Of course, some oil rationing and higher recycling of copper can prolong a few years, the expected shortage of both components, but we are already running against the clock. And let’s not fool ourselves, boost recycling or circular economy, they are patches to buy time, if the decline in production has begun. They do not serve to sustain alone a civilization with increasing demand for all kinds of materials. In any case, they can serve to maintain a much smaller civilization, but it would not be ours, at least with the current parameters.

Bubbles in the markets and excess debt.

At the same time as news of a possible start to the depletion of resources, market bubbles are on track. The Western stock exchange is at historic highs, eliminating once and for all the notion of risk of the equation they share with profitability. If the risk-return binomial once presided over market investment, the irresponsible action of the Central Banks, since the 2008 crisis, has led to the belief that the stock exchanges will never fall hard because the BC will not allow it, intervening quickly to avoid major evils. So, the bag only has one address (upwards, of course). At the same time as this bubble unfolds, we witness an explosion of debt (especially public), where states allow themselves to finance all kinds of payments, knowledgeable of the power of the BC printer.

We are facing unknown times, where the market rewards huge new debt issues, at lower rates (or the forecast of rates downwards). As one expert says, the current bond market is not understood.

Excess debt presides over major economies. The need to generate five dollars of debt for every dollar of GDP growth allows us to believe that the economy continues to grow naturally, when it is not. The outbreak of debt since the 2020 pandemic has been perfectly possible to mask growth that has not been such, but the result of an unpayable debt generation, which artificially drives rates. At the same time, the need to maintain growth (natural or artificial) at all costs leads to instability of the trust system, when the hellish spiral of debt issuance enters, as the only means to pay the debt contracted previously contracted. This vicious circle is the prelude to the destruction of the fiduciary system, when trust in the currency is lost due to the continuous use of the BC printer. The inflation we are enduring is only a reflection of the monetary devaluation due to the abuse of the permanent injection of money, and the difficulty of redirecting inflation figures is still a consequence of the exhaustion of the system, which can only resort to massive indebtedness, as a method of keeping GDP accounting growth intact.

AI, as a growth engine, has replaced the old bubble.com with the new AI bubble. The Nasdaq shows a spectacular graphic as the movement’s technological representative.

Far away is the bubble.com explosion in 2000, with a much larger current bubble and still growing.

Geopolitics

Along with the debt-supply bubble, amplified by the global trust system and at the beginning of the resources depletion phase, the struggle for world hegemony has exploded, partly due to the previous two points, but above all at the end of the expansionary period dominated by the US, after the Second World War. The non-acceptance of a multipolar world, without clear “controller,” is causing multiple conflicts that can lead to a world (military) war. Of course, the trade war has long since broken out, but the formation of two antagonistic blocs (OECD and BRICS) can lead to a confrontation, perhaps prolongation and extension of the current conflicts in Ukraine and the Middle East.

China has focused all its growth on the energy transition (wind-photovoltaic energy, battery manufacturing and electric mobility), basing much of its business on the export of goods related to the energy transition. The application of intimidating tariffs on all these companies-products and the possible extension of the tariff list to the European Union puts the Chinese economy against the ropes. It is a declaration of commercial “war” at all levels and leaves little resources to China to face it. The dynamics of imposing sanctions and their response lead to the fragmentation of world trade into two large blocs.

The replacement of the SWIFT system that controls all transactions in the world, with national or international digital system, can put an end to a system that has lasted more than fifty years, allowing full dominance of trade under the yoke of the dollar.

Another reason to interpret these movements as the top of civilization, as the partition of world trade into two incompatible blocs will reduce world trade and begin a phase of autonomous between blocs. Resources are in one block and technology in the other, but if they cannot be exchanged, the resulting relocation will also bring a loss of competitiveness and a decline in global trade, not to mention the not despicable possibility of war at all levels.

Conclusion.

Therefore, all aspects that affect the zenith of civilization are present and are grouped around specific dates. 2025-2026, should mark the beginning of the end, with a slightly downward phase of plateau until 2030. In any case, I will continue to monitor events to mark the fine setting. Of course, we cannot forget that zenith remains a long process, so few differences will be observed in the fundamental data, for the immediately preceding and subsequent period (2020-2030) to the achievement of zenith. Remember that the fundamental characteristic that the zenith must represent is the decline and by inevitable association, the fall of the capitalist system in force in the West. We all know that this system is incompatible with decline, due to the trend of general deterioration in all economic areas, which are only designed to function in the midst of continuous growth.

Of course, the certification of the zenith can only be reflected very late. It is quite possible that we are only aware of this, after a few years, so the debate will not be definitively closed, until it is completely evident to all, the significant decline in economic activity in the first world.

Basic references to monitor how indicators will be the explosion of bubbles (bag-debt), the obvious fall in oil and copper production, or the beginning of a world war, accompanied by rationing and multiple prohibitions.

I say goodbye with a few words from Tim Morgan, who summed up the situation described in the post, in a couple of sentences.

“The big tacit fact of the 2020s is that the global economy is in the process of moving from growth to contraction and, once again, it is a process that no one can stop, let alone reverse it.”

6 Responses to We have a date for the zenith of civilization: 2025-2026