What the Export Land Model Means for Energy Prices

David Galland, Managing Director Casey Research June 5th, 2008

To understand the importance of exports when discussing peak oil, ask yourself the question: “What’s more important: the fact that global oil production is falling… or that the oil exporting nations are cutting off their exports?”

While the two questions are clearly linked, it is the nuance of the export question that clearly matters the most. Especially if you live in a country such as the U.S., which currently imports about 70% of its oil.

Which brings us to the Export Land Model (or, ELM as I will refer to it from here). The basic thesis expressed by Jeffre J. Brown is that to fully appreciate the impact of peak oil, you can’t just look at the production declines, you also have to look at the rate of local consumption [in the country that exports its oil because if local people use a lot of oil, there’s less oil to export].

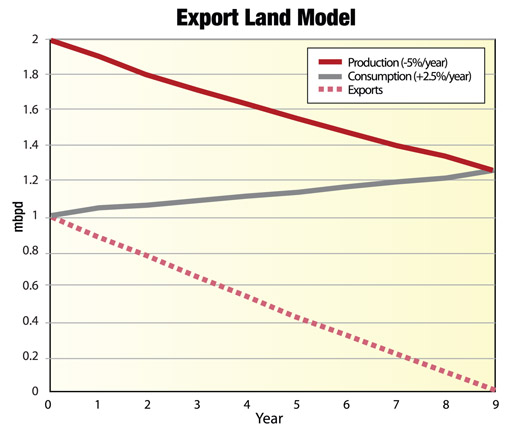

The ELM graph here looks at both sides of the equation, and the result as it applies to exports

As you can see [this chart of ELM] assumes that after a country’s oil production peaks it declines at a rate of 5% per year at the same time local consumption increases by 2.5%. The dashed red line shows the impact that will have on the ability of the country to export its excess production. Using these assumptions, the ELM shows that exports reach zero in 9 years.

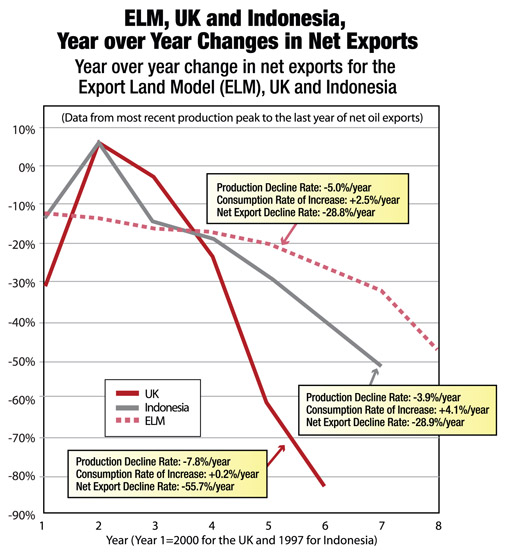

[In the real world the exports may decline much faster than in this example]. The chart below plots the hypothetical ELM against the actual data from the United Kingdom and Indonesia. While the ELM forecast hypothesizes 9 years between peak to the end of exports, Indonesia’s exports ceased 7 years after peak, and the UK’s exports stopped just 6 years after peak.

The important take away here is that the global market is now deprived of these exports; between UK and Indonesia alone, the change over the last decade alone amounts to a swing in the wrong direction of a total of 2 million barrels per day. And those are just two of a number of important countries which have swung from exporters to importers in recent years.

So while people tend to focus on production, they are overlooking the impact on exports forecast by the ELM. China went from a net exporter in 1993 to importing 4 million barrels a day today… with those imports projected to rise another 50% over the next 10 years.

This is what’s creating so much international competition for the remaining supplies of oil. And if the ELM is right, things are about to get far worse.

The Even Bigger Picture

In my interview, I also asked Jeffrey to share his thoughts on the situation globally. Here’s his response.

“Global production peaked in 2005, and we’re now into the third year of decline. And the critical point, to keep in mind, is our model and case histories show that the decline rate accelerates, year by year. Using the Lower 48 in the United States as an example, you can see the annual declines going 2%, 3%, 5%, 7%, 10%, 15%, 20, on and on. So it’s an accelerating decline rate.