Preface. This is a book review of Ehrman’s 2023) Armageddon: What the Bible Really Says about the End. I thought this book was both profound and interesting. I have been trying for years to understand what evangelists are thinking, why they voted for Trump, are easily tricked into being anti-vaccination and so on. And no wonder they are so gullible, they believe in what the Bible says literally, though few have actually read it, or understood what they were reading, which requires knowing history, other languages and more. And also believe whatever their chosen authoritarian leaders and preachers tell them.

If you are interested in critical thinking, it was written by a biblical scholar who is still very devout, and he explains brilliantly what Revelations and other verses in the bible actually mean within their historic context. The apocalypse was clearly meant to be happening back when the chapters were written, not in the future, not today. This book explains how that false idea became popular in the 1800s, and especially with Hal Lindsey’s book The Late Great Planet Earth. And how in this and other books, instead of reading the Bible as a book, verses are randomly taken out of context and strung together to come up with really wacky predictions.

Also, many evangelicals treat the bible like the I Ching, and randomly open it up and read a verse, hoping it will shed light on some problem they’re dealing with.

Preface. It is very hard to find anything on the U.S. military or governments awareness of nuclear winter. So far the only other information I’ve found on this is from 2023 Risk Analysis methods for nuclear war & nuclear terrorism. National Academies of Sciences. DOI 10.17226/26609

Many details about the consequences of nuclear explosion–produced soot remain uncertain, but a key point is that, to this committee’s knowledge, this topic has not been extensively studied by the U.S. government, especially regarding the impact on highly interconnected, technologically dependent modern society, as well as on climate. There is a need to improve the understanding of less-well- understood physical effects of nuclear weapons (such as fires; damage in modern urban environments; electromagnetic pulse effects; and climatic effects, such as nuclear winter), as well as the assessment and estimation of psychological, societal, and political consequences of nuclear weapons use.

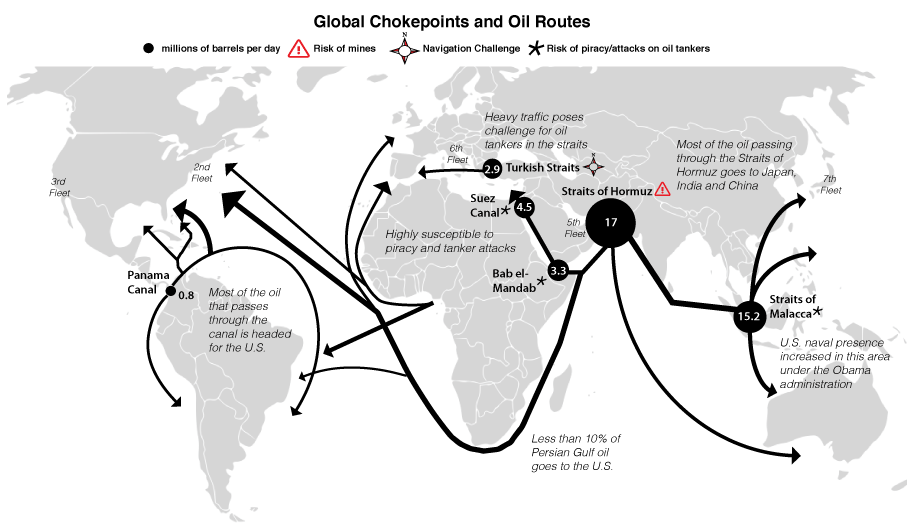

Preface. Below are several articles I’ve collected since 2005 on oil chokepoints. If oil tanker traffic were stopped on one or more, much of the world would plunge into a financial and energy crisis.

The U.S. has been far less vulnerable to shortages of Middle Eastern oil than the rest of the world by having our own oil and diversifying to Central & South American, Canadian, and other sources.

But that is changing. World oil peaked in 2018, and fracking will likely peak from 2024 to 2029. The U.S. and all other nations will become more dependent on OPEC, with 82% of remaining conventional oil reserves. Conventional is easier and cheaper than fracked, tar sands, or Venezuelan oil which cost much more to obtain plus need expensive refining (Newman 2018).

China and Southeast Asia have more glittery gadgets to sell in exchange for the remaining oil in the Middle East, and their blue navy is the strongest in the world and much closer to the Middle East. Because the U.S. restarted the Cold War arms race, China has gone from 200 nuclear missiles in 2020 to 1500 by 2030 (the U.S. has about 5,000 of the 13,000 nuclear missiles in the world). Since just 100 bombs dropped by any nation(s) would create a nuclear winter that would kill up to 5 billion people, the consequences of a chokepoint being blocked increases the chance of nuclear war.

Piracy and chokepoints in the news:

2021 Pirates Plague Mexico’s Offshore Oil Platforms: Incidents of piracy in the Mexican waters in the Gulf of Mexico have led to calls to Mexico’s Navy to increase its presence in the area where pirate attacks on vessels and oil platforms have been rising. Last month armed thieves attacked the Sandunga oil platform in the Bay of Campeche, stole equipment and belongings of rig workers, and fled with speed boats and there have been another 11 serious incidents against ships in the first half of 2020 alone.

Asian nations will be most affected if war closes the straits of Hormuz

60% percent of America’s oil arrives on vessels.

Due to the narrowness of the straits all of them can be disrupted with relative ease by piracy, terrorism, wars, or shipping accidents, affecting the supply of oil and world prices.

The strong dependence of the U.S. economy on oil has made it of the utmost importance to guarantee the free flow of shipments through these straits. For this reason policing has fallen mainly on the U.S. Navy with the help of some allies. Cost estimates of maritime patrolling for the U.S. have been calculated to range between $68 and $83 billion per year, or 12 to 15 percent of conventional military spending. The rest of the world has benefited freely from this security provided by the U.S.

As long as the U.S. economy continues to depend heavily on oil it will have to incur in the high maritime patrolling costs to guarantee the free flow of oil through these critical straits.

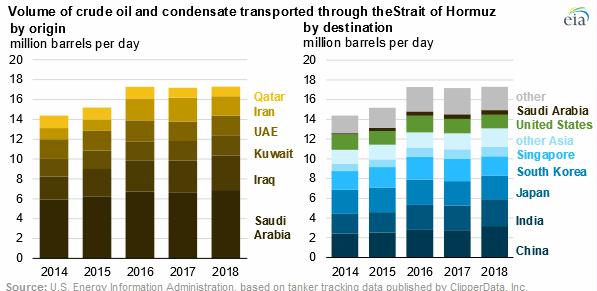

According to John Hofmeister, former president of Shell Oil, “With respect to the choke points, the three most serious are the Suez Canal, the Hormuz Straits, which is separating Yemen from Oman and Iran, and the Straits of Malacca, which is between Malaysia and Indonesia. These choke points carry enormous amounts of crude oil. Matt Simmons used to speak of the Straits of Hormuz as, we live one day away from an oil Pearl Harbor. In other words, those Straits of Hormuz transport between 20 and 25% of daily consumption of global oil, and were they to be shut in, the world would be in a panic overnight if it were not possible to pass oil.

The Straits of Hormuz watch about 20 to 25% of the world’s daily crude oil production move through it, and if the world were to lose that amount of oil because of a shutdown in the Straits, I think that the immediate impact on crude oil prices would be to not just double but even triple the current crude oil price of the panic that would set in in terms of future contracting. There might be a slight delay to see how long it make take to clean up the mess that might be created there but it is such a critical pinch point and there is so much of that oil that goes both east and west that it is not only energy security for the United States, it is energy security for the world’s second largest economy, China. And so the consequence would be dramatic. Five dollars would look cheap in terms of a gasoline price in the event of the Straits of Hormuz being shut in.” (Serial No. 112-4).

Attack on Abqaiq

The National Commission on Energy Policy and Securing America’s Energy Future conducted a simulation called Oil Shock Wave to explore the potential security and economic consequences of an oil supply crisis. The event started by assuming that political unrest in Nigeria combined with unseasonably cold weather in North America contributed to an immediate global oil supply shortfall. The simulation then assumed that 3 terrorist attacks occur in important ports and processing plants in Saudi Arabia and Alaska which sent oil prices immediately soaring to $123 a barrel and $161 barrel 6 months later. At these prices, the country goes into a recession and millions of jobs are lost as a result of sustained oil prices. This simulation almost became reality with the failed attack on Abqaiq in Saudi Arabia in February 2006. Had the attack been successful, it would have removed 4to 6 million barrels per day from the global market sending prices soaring around the world and would likely have had a devastating impact on our economy. (Indiana Senator Evan Bayh, U.S. SENATE March 7, 2006. Energy independence S. HRG. 109-412)

Keating, J. July 17, 2014. The Middle East Friendship Chart. slate.com

Ras Tanura port in Saudi Arabia: 10% of the world’s oil

Saudi Arabia had 22% of the world’s oil reserves (in 2005) The largest oil terminal in the world is Ras Tanura, on the east coast of Saudi Arabia, along the Persian Gulf. Ras Tanura is the funnel through which nearly 10 percent of the world’s daily supply of petroleum flows. In the control tower, you are surrounded by more than 50 million barrels of oil, yet not a drop can be seen.

As Aref al-Ali, my escort from Saudi Aramco, the giant state-owned oil company, pointed out, ”One mistake at Ras Tanura today, and the price of oil will go up.” This has turned the port into a fortress; its entrances have an array of gates and bomb barriers to prevent terrorists from cutting off the black oxygen that the modern world depends on. Yet the problem is far greater than the brief havoc that could be wrought by a speeding zealot with 50 pounds of TNT in the trunk of his car. Concerns are being voiced by some oil experts that Saudi Arabia and other producers may, in the near future, be unable to meet rising world demand. The producers are not running out of oil, not yet, but their decades-old reservoirs are not as full and geologically spry as they used to be, and they may be incapable of producing, on a daily basis, the increasing volumes of oil that the world requires. ”One thing is clear,” warns Chevron, the second-largest American oil company, in a series of new advertisements, ”the era of easy oil is over.”

If consumption begins to exceed production by even a small amount, the price of a barrel of oil could soar to triple-digit levels. This, in turn, could bring on a global recession, a result of exorbitant prices for transport fuels and for products that rely on petrochemicals — which is to say, almost every product on the market. The impact on the American way of life would be profound: cars cannot be propelled by roof-borne windmills. The suburban and exurban lifestyles, hinged to two-car families and constant trips to work, school and Wal-Mart, might become unaffordable or, if gas rationing is imposed, impossible.

Ghawar is the treasure of the Saudi treasure chest. It is the largest oil field in the world and has produced 55 billion barrels of oil the past 50 years, more than half of Saudi production in that period. The field currently produces more than five million barrels a day, about half of the kingdom’s output. If Ghawar is facing problems, then so is Saudi Arabia and, indeed, the entire world.

Simmons found that the Saudis are using increasingly large amounts of water to force oil out of Ghawar. “Someday the remarkably high well flow rates at Ghawar’s northern end will fade, as reservoir pressures finally plummet. Then, Saudi Arabian oil output will clearly have peaked Simmons says that there are only so many rabbits technology can pull out of its petro-hat.

Strait of Hormuz

Any military action in the Strait of Hormuz in the Gulf would knock out oil exports from OPEC’s biggest producers, cut off the oil supply to Japan and South Korea and knock the booming economies of Gulf states.

Roger Stern, a professor at the University of Tulsa National Energy Policy Institute, estimates we’ve spent $8 trillion protecting oil resources in Persian Gulf since 1976, when the Navy first began increasing its military presence in the region following the first Arab oil embargo. We did this because we feared oil supplies would run out, and that the Soviets would march to the Persian gulf to get oil when they ran low themselves (Stern). We import very little of this oil, yet Japan, Europe, India, and the nations that do don’t pay us to do this. Admiral Greenert plans to shift 10% of our navy from the East Coast to the Pacific Coast to protect the South china seas (from China).

Here are some key facts on what passes through the international waterway and some of the direct economic consequences of any attack on merchant shipping.

20 percent of the world’s oil traded worldwide (35% of all seaborne oil), and 20% of the global liquefied natural gas (EIA).

2.9 billion deadweight tons passes through the strait every year.

Crude oil exported through the Strait rose to 750 million tons in 2006.

27 percent of transits carry crude on oil tankers, rising to 50 percent if petroleum products, natural gas and Liquefied Petroleum Gas transits are included.

Transits for dry commodities like grains, iron ore and cement account for 22 percent of transits.

Container trade accounts for 20% of transits, carrying finished goods to Gulf countries.

Oil exports passing through Hormuz: (2006 figures)

Saudi Arabia — 88 percent

Iran — 90 percent

Iraq — 98 percent

UAE — 99 percent

Kuwait — 100 percent

Qatar — 100 percent

Top 10 importers of crude oil through Hormuz (2006 figures)

Japan — Takes 26% of crude oil moving through the strait (shipments meet 85% of country’s oil needs)

Republic of Korea — 14 percent (meets 72 percent of oil needs)

United States — 14 percent (meets 18 percent of oil needs)

India — 12 percent (meets 65 percent of oil needs)

Egypt — 8 percent (N.B. most transhipped to other countries)

U.S. Energy Security Strait of Hormuz Threat – All OPEC imports from the Persian Gulf region are shipped via marine tankers through the Strait of Hormuz. Due to Iran’s developing nuclear arms program and Israel’s perception of this being a threat, which could lead to conflict if Israel makes a first strike against Iran (regardless of whether the threat is verified or not), and U.S. sanctions to possibly curtail Iran’s nuclear arms development, Iran has threatened to the shutdown of the Strait of Hormuz in retaliation. If and when Iran carries out their threat to shutdown the Strait of Hormuz the U.S. would immediately lose about 2.2 MBD of crude oil imports or almost 12% of current total petroleum oil supplied (consumed); far greater than the 4% lost during the 1973 Arab OPEC oil embargo.

Strait of Hormuz Shutdown Impacts – The impact of losing all Persian Gulf imports could be substantial. Not only would the U.S. be subjected to a very quick loss of 2.2 MBD of imports, but the impact on world markets could also be devastating (up to 20% of all world market crude oil supplies currently flow through the Strait). World oil prices could directionally double almost overnight, sending world energy markets and economies into chaos. While the U.S. and UN conventional military forces should be able to readily take-on and neutralize Iran’s conventional forces, it’s Iran’s small-independent, unconventional forces that likely pose the greatest and longer term threat to Persian Gulf shipping and regional OPEC oil infrastructures.

Other Chokepoints (EIA)

Strait of Malacca with 17% of the world’s oil, most of it headed to China, Japan and South Korea.

Suez Canal / SUMED pipeline with 5% of world oil, key routes for oil destined for Europe and North America. A potential threat is the growing unrest in Egypt since their revolution in 2011.

Bab el-Mandab could keep tankers from the Persian gulf from reching the Suez canal and sumed pipeline

Turkish Straits. Increased oil exports from the Caspian Sea region make the Turkish Straits one of the most dangerous choke points in the world supplying Western and Southern Europe.

Danish Straits, an increasingly important route for Russian oil to Europe.

Serial No. 112-4. February 10, 2011. The effects of middle east events on U.S. Energy markets. House of Representatives, subcommittee on energy and power 112th congress. 231 pages

Semple K (2020) Piracy Surges in Gulf of Mexico, Prompting U.S. Warning. There have been scores of attacks in Mexican waters, taxing the country’s overstretched security forces. New York Times.

Preface. This contains excerpts from a post by two of the leading nuclear winter scientists and is a good summary of the situation. There is also a section on what can be done, how you can help. Nuclear winter is a double whammy, it is also extreme climate change and is a smaller version of the asteroid that wiped out the dinosaurs 65 million years ago with smoke high in the atmosphere that cooled the Earth for a decade or more. Several papers have found that up to 5 billion people might die.

But nuclear winter is not a consideration in arms control or a spur to get arms reduction talks going. What could be a higher priority? No, instead the U.S. started an arms race when it decided to upgrade our nuclear missiles, submarine fleet and more. China had 200 bombs in 2020, but now plans to have 1500 by 2035 to counter the U.S. buildup of our nuclear arsenal.

I very much recommend this 8 minute (4 on 2x speed) video to give you an idea of how absolutely insane and dangerous our nuclear policies are

Robock A, Prager SC (2021) Geoscientists Can Help Reduce the Threat of Nuclear Weapons. A nuclear war would claim many lives from its direct impacts and cause rapid climate change that would further imperil humanity. Scientists can help shape policies to put us on a safer path. EOS. https://doi.org/10.1029/2021EO210633

While we all recognize that global warming threatens humanity, the effects of nuclear war pose an even graver threat to the global population.

The immediate devastation from nuclear blasts and subsequent fires and the lasting harm from nuclear radiation have, of course, been demonstrated tragically. But a nuclear war would also produce nearly instantaneous climate change that among other effects, would threaten the global food supply. Even a regional nuclear war could threaten civilization globally and condemn innocent bystanders to famine, including inhabitants of the country that initiated the conflict. In effect, a nuclear attack would be the actions of a suicide bomber [Robock and Toon, 2012].

The scientific community, particularly physicists and geophysicists, has a special relationship with the problem of nuclear weapons. We have performed the research and developed the technology that created the weapons, and we have studied their effects. But there is also a long history of scientists opposing use of the weapons and warning of the outcomes in the event they are used. Today, as nuclear arsenals and the plausibility of their use are growing anew, we argue that it is again time for physical scientists to advocate for steps that reduce the nuclear threat. A new coalition is working to do just that.

The Growing Threat

The existence of nuclear weapons means that they can be used, and this threat is getting more severe as the number of possible scenarios leading to nuclear war rises. Currently, there are more than 9,000 nuclear warheads in the active military stockpiles of nine nations, with more than 90% of those in Russia and the United States. Nearly 2,000 warheads are on alert status, ready to launch within minutes of an order.

New technologies threaten the abilities of governments to control and secure nuclear weapons. A cyberattack on nuclear weapons control systems, for example, could create false warnings of launches or perhaps even initiate real launches. Even before the emergence of cyberthreats, there were many instances of near launches by technical or human error. And it was only because cooler heads prevailed that nuclear weapons were not used deliberately during the Cuban Missile Crisis in 1962 or amid the Vietnam War when military leaders urged their use [Ellsberg, 2017].

The nuclear arms control regime has been weakened in recent years with the termination of the Anti-Ballistic Missile Treaty and the Intermediate-Range Nuclear Forces Treaty between Russia and the United States, the withdrawals of those countries from the Treaty on Open Skies, and the withdrawal of the United States from the Iran nuclear deal. These actions are culminating in an emerging nuclear arms race, with most nuclear powers modernizing their nuclear arsenals. The planned trillion-dollar, multidecade modernization of the nuclear arsenal in the United States would commit the country to nuclear weapons for most of this century.

Nuclear Climate Change

In addition to immense physical damage to both built and natural environments, as well as lingering radioactive fallout, a nuclear conflict would cause rapid changes in Earth’s climate. Smoke from firestorms ignited by attacks on cities and industrial areas would rise into the stratosphere and persist for years. Smoke from firestorms ignited by attacks on cities and industrial areas would rise into the stratosphere and persist for years [e.g., Yu et al., 2019]. This smoke would block sunlight, causing global cooling [Robock et al., 2007a; Coupe et al., 2019], and it would lead to stratospheric ozone depletion that would enhance the amount of ultraviolet radiation reaching Earth’s surface [Bardeen et al., 2021].

The original suggestions of “nuclear winter” following a nuclear war by Turco et al. [1983] and Aleksandrov and Stenchikov [1983], which were based on very simple climate models, have been supported strongly by recent work using modern high-resolution general circulation models to simulate and predict its effects [Robock et al., 2007a; Coupe et al., 2019]. Even a regional nuclear war, such as between India and Pakistan [Robock et al., 2007b; Toon et al., 2019], in which less than 3% of the world’s nuclear weapons were detonated, would suddenly decrease the average global temperature by 1°C–7°C, precipitation by up to 40%, and sunlight by up to 30%. No matter the scale of the soot injection into the skies, the multiyear lifetime of smoke in the stratosphere means the effects on climate would last a decade, with the largest impacts continuing for more than 5 years. Such a conflict would decrease crop production to an extent that it could seriously threaten world food security and even trigger global famine [Jägermeyr et al., 2020; L. Xia et al., Global famine after nuclear war, submitted to Nature Food, 2021].

A Safer Path

There are many measures that can be implemented to reduce the likelihood of using nuclear weapons, including steps by the United States that in our view would make the country and the world safer. For example, we can adopt a no-first-use policy, meaning the United States would never start a nuclear war but, rather, only respond to a nuclear attack. We can also eliminate the launch-on-warning option, which pressures a presidential decision on whether to launch a counterattack within 5–10 minutes (and is thus particularly vulnerable to launches by error), and we can eliminate presidential sole authority to launch nuclear weapons. This most fateful decision should not be made by just one person [Perry and Collina, 2020]. In addition, we can and should restart the arms reduction negotiations between the United States and Russia that were initiated by President Ronald Reagan and Soviet leader Mikhail Gorbachev in the 1980s. These negotiations led to multidecade reductions in nuclear arsenals, but that progress has recently stalled.

We believe that the ultimate solution to the problem of nuclear weapons is to ban them globally. In 2017, the International Campaign to Abolish Nuclear Weapons led the effort to have the Treaty on the Prohibition of Nuclear Weapons signed at the United Nations. The campaign was awarded the 2017 Nobel Peace Prize “for its work to draw attention to the catastrophic humanitarian consequences of any use of nuclear weapons and for its ground-breaking efforts to achieve a treaty-based prohibition of such weapons.” The treaty came into force on 22 January 2021 after a 50th nation ratified it. Although the nuclear powers are not yet party to it, the treaty, which prohibits development, testing, possession, and use of nuclear weapons, nonetheless sets a new norm and direction for the future, much like existing treaties that prohibit the use of chemical weapons, biological weapons, land mines, and cluster bombs.

Because the “catastrophic humanitarian consequences” include not only the horrific direct effects but also potential impacts on climate and food supplies, physical scientists, including geoscientists, can offer expertise and insight into the hazards and consequences of nuclear conflict—and can be influential voices for nuclear threat reduction. In fact, at three international conferences, in 2013 and 2014, focused on the humanitarian impacts of nuclear war, participating climate scientists helped to push authorities from nonnuclear nations to sign and ratify the 2017 treaty.

Scientists have organized together in the past to exert pressure effectively on governments. Soon after physicists developed nuclear weapons in the 1940s, many then organized to warn of the dangers of nuclear arms. For example, James Franck and others published a report in June 1945 arguing against the use of a nuclear weapon in Japan; Albert Einstein led the Emergency Committee of Atomic Scientists, formed in 1946, to warn the public and mobilize scientists; and Niels Bohr urged world leaders, including Franklin Roosevelt and Winston Churchill, to preempt a postwar arms race. Through the Cold War, many scientists worked toward arms control and cooperative security. Geophysicists developed technologies to detect underground and atmospheric nuclear tests (sensors that as a by-product, have also been used to collect Earth observations). And in the mid-1980s, American and Russian climate scientists together warned Reagan and Gorbachev of the likely effects of a nuclear winter, helping to end the nuclear arms race. Recently, the U.S. physics community has again taken steps to influence U.S. nuclear policy—and geoscientists have the chance to join and work together with this community.

Influential Voices

In 2020, the American Physical Society (APS) initiated the Physicists Coalition for Nuclear Threat Reduction with the goal of creating a national network of physical scientists to advocate for nuclear threat reduction. A supporting goal is to inform the physical science community about nuclear arms issues. In its first year, the Physicists Coalition’s initial 13-member project team held more than 60 colloquia in physics departments and national laboratories around the country to provide an overview of the nuclear arms challenge and to introduce the community to the coalition. The program of colloquia is ongoing, and we continue to present webinars on specific arms control topics.

Our advocacy work includes a broad array of actions but focuses on contacts and meetings with congressional representatives and staff. Throughout 2020, the coalition, along with other groups, successfully advocated to Congress not to approve a resumption of nuclear testing, which had been suggested by some legislators, and for the president to extend the New START Treaty, which limits the number of strategic nuclear weapons deployed by the United States and Russia. Soon after assuming the presidency, Joe Biden agreed with President Vladimir Putin to extend the treaty for 5 years. Now the coalition’s focus is on advocating for the country to adopt a no-first-use policy, meaning its nuclear arsenal would remain only as a deterrent to attack. Pulling the option of first use by the United States off the table can reduce geopolitical tensions that could lead to war.

The Physicists Coalition for Nuclear Threat Reduction welcomes all physical scientists, including those working in engineering science, to join, and we encourage you to host a colloquium, funded by the coalition, at your institution. The coalition offers an opportunity to be part of a movement specifically targeted at one of humanity’s most existential threats. We must solve the problem of nuclear weapons so that we have the luxury of devoting our time to solving the climate crisis.

Aleksandrov, V. V., and G. L. Stenchikov (1983), On the modeling of the climatic consequences of the nuclear war, in Proceedings on Applied Mathematics, 21 pp., Comput. Cent., Russ. Acad. of Sci., Moscow.

Bardeen, C. G., et al. (2021), Extreme ozone loss following nuclear war results in enhanced surface ultraviolet radiation, J. Geophys. Res. Atmos., 126(18), e2021JD035079, https://doi.org/10.1029/2021JD035079.

Coupe, J., et al. (2019), Nuclear winter responses to nuclear war between the United States and Russia in the Whole Atmosphere Community Climate Model Version 4 and the Goddard Institute for Space Studies ModelE, J. Geophys. Res. Atmos., 124(15), 8,522–8,543, https://doi.org/10.1029/2019JD030509.

Ellsberg, D. (2017), The Doomsday Machine: Confessions of a Nuclear War Planner, 420 pp., Bloomsbury, New York.

Jägermeyr, J., et al. (2020), A regional nuclear conflict would compromise global food security, Proc. Natl. Acad. Sci. U. S. A.,117(13), 7,071–7,081, https://doi.org/10.1073/pnas.1919049117.

Perry, W. J., and T. Z. Collina (2020), The Button: The New Nuclear Arms Race and Presidential Power from Truman to Trump, 256 pp., BenBella Books, Dallas, Texas.

Robock, A., and O. B. Toon (2012), Self-assured destruction: The climate impacts of nuclear war, Bull. At. Sci., 68(5), 66–74, https://doi.org/10.1177/0096340212459127.

Robock, A., L. Oman, and G. L. Stenchikov (2007a), Nuclear winter revisited with a modern climate model and current nuclear arsenals: Still catastrophic consequences, J. Geophys. Res. Atmos., 112, D13107, https://doi.org/10.1029/2006JD008235.

Robock, A., et al. (2007b), Climatic consequences of regional nuclear conflicts, Atmos. Chem. Phys., 7(8), 2,003–2,012, https://doi.org/10.5194/acp-7-2003-2007.

Toon, O. B., et al. (2019), Rapidly expanding nuclear arsenals in Pakistan and India portend regional and global catastrophe, Sci. Adv., 5(10), eaay5478, https://doi.org/10.1126/sciadv.aay5478.

Yu, P., et al. (2019), Black carbon lofts wildfire smoke high into the stratosphere to form a persistent plume, Science, 365(6453), 587–590, https://doi.org/10.1126/science.aax1748.

Preface. Of all the hundreds of obstacles fusion has yet to overcome, its death knell could be as simple as a shortage of the essential fuel it runs on: tritium. Yes, there are some kinds of imaginary fusion reactors that don’t need it, but they require a billion degrees Celsius (1.8 billion F) of heat. Tritium fusion reactors require a “mere” 150 million degrees Celsius (270 million Fahrenheit).

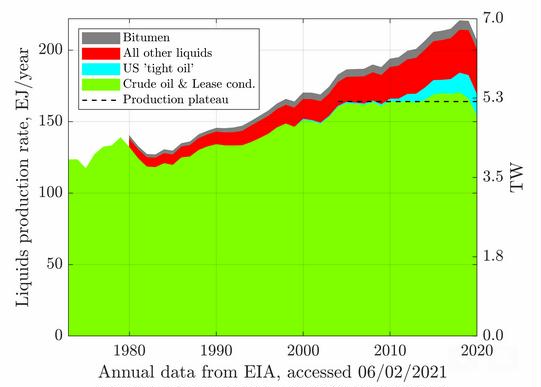

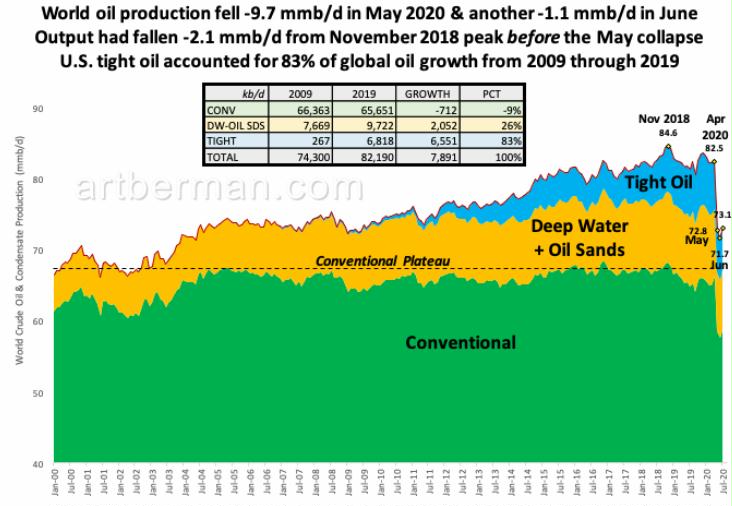

Preface. When I first published this post in February of 2022, I said that peak world oil production might have arrived, but it takes 5 years in the rear-view mirror to call it. Now peak “crude oil including lease condensate oil” is officially here! Production was less in November 2023 than the peak of global oil production in November 2018. See for yourself at the U.S. Energy Information Administration site here.

You can ignore all the other liquids, they do not make diesel fuel for heavy-duty trucks, locomotives, and ships that do the actual work of civilization. Mainly the other categories are good for plastics, which we have more than enough of. Or ethanol for gasoline, but you’d destroy a diesel engine if you added this to extend diesel fuel. I suspect these categories were added to keep people from panicking like they did in the oil crises of 1973 and 1979. Why would they panic? There is a very tight correlation between fossil production, GDP, and population.

Unconventional shale oil was responsible for over 90% of the increased production above the 2008 plateau with a little help from Canadian tar sands.

Seven of the eight U.S. shale basins are past peak, with only the Permian producing the majority of fracked oil. And it may peak in 2024 (Geiger 2022). Or not, some scientists think the USA shale oil production could be on a plateau until 2040. But at any rate, when shale oil and gas decline, will be a hell of a rollercoaster ride down, since shale oil declines 80% over 3 years. And already 81% of all the other oil production is declining at 8.5% a year, offset by 4.5% enhanced oil recovery.

As the energy crisis in Europe deepens, there could be a sudden mad rush of capital to explore, drill, and produce more oil which would keep the plateau going a bit longer.

But wars, natural disasters, the export land model (the few oil producing nations left keep the oil for their own population and factories), plus other factors and black swans could also throw a monkeywrench in the works and cause oil production to fall rapidly.

Above all, it is the FLOW rate that matters. Half the oil may still be underground, but it will take longer and more expensive to get, and require more energy to extract, subtracting what can be delivered to society for other uses. Delannoy et al (2021) estimate that by 2050, half of the gross energy output will be engulfed in its own production. Whoa — if the EROI of civilization needs to be at least 10 to 14, that’s the end of civilization (Lambert et al 2014)!

Also important is that the actual problem is Peak Diesel since this is the portion of an oil barrel that really matters, as I showed inWhen Trucks Stop Running: Energy and the Future of Transportation. Diesel is what powers tractors, harvesters, mining, long haul, construction, and myriad other trucks that do the actual work of civilization. Diesel production may have peaked in 2015 (Turiel 2021) and Russia’s invasion of Ukraine has led to shortages of diesel (Slav 2022). In addition, supply chain issues for goods are likely to increase since trucks make everything you own or can imagine possible, and energy decline will lead to a financial depression, business failures, and a lack of key spare parts for trucks of all kinds (as well as locomotives and ships, which carry 90% of all internationally traded goods, including oil).

And there may be a lot less oil than the EIA, IEA, BP Statistical review, and other estimates of world reserves have estimated. Laherrere et al (2022) explain the various methods used to calculate world fossil reserves, and why their method is probably most accurate — which is what Laherrere has written about for the past 60 years. Many geologists who’ve modeled likely fossil fuel decline within the IPCC climate model predicted that the most likely outcomes were RCP 2.6 to 4.5 (see the last chapter in “Life After Fossil Fuels”). If 2018 was the world peak oil production year, perhaps the lower RCP 2.6 is most likely. Laherrere et al (2022) estimates RCP 3.0 since the global CO2 emissions for the period 2020–2100 are approximately 1000 GtCO2 for coal, 750 GtCO2 for oil and 650 GtCO2 for natural gas, giving a grand total of 2400 GtCO2, with a further ~850 GtCO2 being emitted beyond 2100. Clearly such emissions are incompatible with the 580 GtCO2 limit to CO2 emissions to 2100 assumed by Welsby et al 2021 to meet 1.5 °C goal in the 2022 IPCC report. If the 1750 GtCO2 emitted so far has led to a 1.1 C increase, 3250 GtCO2 would add another 2 C for a total of 3 C above pre-industrial levels.

I think a great deal of oil will be left in the ground. Geology isn’t the whole issue. Oil makes all other resources possible, including food, so its decline is likely to lead to social unrest, depressions, war and civil wars, supply chain failures, natural disasters like hurricanes taking out offshore oil platforms, floods and earthquakes damaging refineries, and other catastrophes that disrupt oil production. And don’t forget that the FLOW RATES will be lower. Maybe the last oil will take 1,000 years to get out — if we can maintain the level of technology we have now when things are falling apart. Nor are unconventional tar sands (Canada) or heavy oil (Venezuela) likely to produce much oil since their energy return on invested is very low. So that leaves their estimate of remaining conventional oil of 1100 Gb (Table 1) to carbon of ~470 GtCO2, well under the 580 GtCO2 limit to CO2 emissions and if the above parameters occur, less coal and natural gas as well.

The end of the boom is in sight for America’s fracking companies. Less than 3½ years after the shale revolution made the U.S. the world’s largest oil producer, companies in the oil fields of Texas, New Mexico and North Dakota have tapped many of their best wells. If the largest shale drillers kept their output roughly flat, as they have during the pandemic, many could continue drilling profitable wells for a decade or two, according to a Wall Street Journal review of inventory data and analyses. If they boosted production 30% a year—the pre-pandemic growth rate in the Permian Basin, the country’s biggest oil field—they would run out of prime drilling locations (the “sweet spots”) in just a few years. For years, frackers told investors they had secured enough drilling spots to keep going for decades. But the limited inventory suggests that the era in which U.S. shale companies could quickly flood the world with oil is receding, and that market power is shifting back to other producers, many overseas. Big shale companies already have to drill hundreds of wells each year just to keep production flat. Shale wells produce prodigiously early on, but their production declines rapidly. The Permian is expected to be the longest-lived U.S. oil region and is home to more than 80% of the country’s remaining economic drilling locations.

2021 The Incredible Shrinking Oil Majors“… the future for these companies has gone from challenged to incredibly bleak. Over the last 20 years, oil supermajors Exxon, Chevron, Royal Dutch Shell and Total have found it challenging to maintain their reserve base and production level. Even though upstream capital spending has surged, production and reserves have persistently declined. Things look significantly worse if you focus only on crude oil. While Exxon’s crude oil production has declined by 8% over the last 20 years (in line with gas production), Royal Dutch Shell’s crude production has collapsed by 20% while Chevron’s has fallen by 7%. While Total is once again the only company to show any growth, it has been modest: oil production is up 0.8% CAGR over the last 20 years. Proved oil reserves tell a similar story. Exxon’s proved oil reserves are down 26% while Royal Dutch Shell’s have collapsed by 57% and Chevron’s have fallen 29%. Even Total’s proved oil reserves have contracted by 16% since 2000. While all four supermajors saw their total proved R/P ratios fall by 26% on average, their oil-only proved Reserves/Production ratios fell by 30%.”

2019. When will ‘peak oil’ hit global energy markets? dw.com. Darren Woods, CEO of ExxonMobil predicts a 25% rise in global energy demand for the next two decades, due to “global demographic and macroeconomic growth trends. When you factor in depletion rates, the need for new oil grows at 8% a year,” he told analysts in March.

FYI, if you’re curious about what oil looks like, go here.

****

Conventional world crude oil production leveled in 2005, and peaked in 2008 at 69.5 million barrels per day (mb/d) according to Europe’s International Energy Agency (IEA 2018 p45). We get 90% of our petroleum from conventional oil.

Source: Tad Patzek.

The U.S. Energy Information Agency shows global peak crude oil production in 2018 at 82.5 mb/d because they included unconventional tight oil, oil sands, and deep-sea oil.

Nor will we ever reach “peak oil demand” because heavy-duty transportation (trucks, locomotives, ships), manufacturing, the 500,000 products made out of petroleum, and natural gas fertilizer that keeps 4 billion of us are utterly dependent on fossil fuels. Even the electric grid depends on fossil fuels to provide two-thirds of electricity, and nearly all of the energy to construct wind and solar contraptions (they are ReBuildable, NOT renewable). This is explained in great detail in my latest book “Life After Fossil Fuels: A Reality Check on Alternative Energy” and previous book” When Trucks Stop Running: Energy and the Future of Transportation”

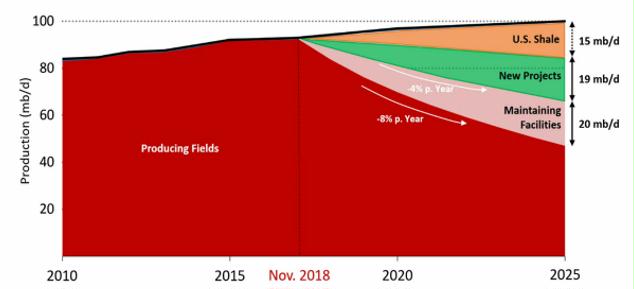

The IEA forecast a supply crunch by 2025 in their rosy and unrealistic New Policies scenario, which assumes greater efficiencies and alternative fuels and electric cars are adopted (Figure 1). By 2025, with 81% of global oil declining at up to 8% percent a year (Fustier 2016, IEA 2018), 34 mb/d of new output will be needed, and 54 mb/d if facilities aren’t maintained. That is more than three times Saudi Arabian production. The 15 mb/d of predicted U.S. shale isn’t likely — indeed, the IEA shows it declining in the mid-2020s (IEA 2018 Table 3.1).

The IEA (2018) points out that the new conventional crude projects approved over the last three years are only half the amount needed by 2025. With Covid-19, few projects are likely to begin. Oil prices have gone down so much that exploration and production investments were plummeting before Covid-19 and many fields already found are too costly to develop. Already four years of world oil consumption, 125 billion barrels, are likely to be written off by oil companies and remain in the ground (Rystad 2020, Hurst 2020).

Figure 1. Expected decline of oil production (red area) and possible stopgaps to the decline rate of 4 to 8% a year. Maintaining facilities refers to enhanced recovery from existing fields (IEA 2018). Modified figure 1.19 from IEA.

Political shortages are as big a problem as geological depletion. At least 90% of remaining global oil is in government hands, especially Saudi Arabia and other countries in the middle east that vulnerable to war, drought, and political instability. Over two-thirds of the remaining oil is in the Middle East, and as populations keep growing there, less oil will be exported as well.

About a quarter of the remaining oil is in the arctic, and will be difficult and extremely expensive to develop due to land permafrost soils and icebergs offshore (see the posts here for details).

And don’t look to offshore oil either, many new offshore projects have even been put on hold. “Between low demand, soaring inventories, depressed prices, a global pandemic, and now, hurricane season, it seems a perfect storm is forming around the offshore oil industry. The world’s offshore oil market, responsible for 30 percent of all the world’s oil production, is facing an impossible set of challenges. With oil sitting at half the price of its yearly high, companies are struggling to rein in capital spending and are beginning to rethink the future of key projects. The crisis has pushed much of the world’s oil production onshore in favor of more flexible rigs and lower operational costs. Many firms operating offshore rigs have yet to recuperate from the last oil price collapse in 2014-2015 when prices fell from $100 to below $40, weighing on the entire industry. Offshore drillers and offshore vessel providers will generally be unable to pay their total outstanding debt of 2020 based on their cash flow from operating activities, unless they are able to make sufficient capital expenditure cuts (Kern 2020).

Saudi Aramco’s chief executive officer, Amin Nasser, said that the company expects to boost its oil production capacity to 13 million barrels per day (bpd) by 2027 from 12 million bpd now. This claim is doubtful.

At the beginning of 1989, Saudi Arabia claimed proven oil reserves of 170 billion barrels. Only a year later, and without the discovery of any major new oil fields, the official reserves estimate had somehow increased by 51.2% to 257 billion barrels. Shortly thereafter, it increased again to 266 billion barrels or so, and in 2017 to 268.5 billion barrels. On the other side of the supply-demand equation, from 1973 to the end of last week, Saudi Arabia pumped an average of 8.162 million barrels per day of crude oil. Therefore, taking 1989 as a starting point (with 170 billion of crude oil reserves officially claimed in that year), in the subsequent 32 years Saudi Arabia has physically pumped and removed forever, a total of 95,332,160,000 barrels of crude oil. Over the same period, there has been no significant discovery of major new oil fields. Despite this, Saudi Arabia’s crude oil reserves have not gone down, but rather have actually gone up. This is a mathematical impossibility on this scale.

Next up – spare capacity. The EIA defines spare capacity very specifically as production that can be brought online within 30 days and sustained for at least 90 days. Saudi Arabia stated for decades that it had a spare capacity of between 2.0 and 2.5 million bpd. This implied – given the widely accepted (but also wrong, as highlighted above) belief that Saudi had pumped an average of around 10 million bpd for many years – that it had the capability to ramp up its production to about 12.5 million bpd in the event of unexpected disruptions elsewhere. This is almost the same level as Nasser’s most recent statement. However, as the 2014-2016 Oil Price War dragged on and reached new heights of economic devastation both for Saudi Arabia and its OPEC brothers, the Kingdom could on average produce no more than just about 10 million bpd – very rarely managing to hit above 10.5 million bpd in the two-year duration of the War.

The obvious question was a simple one: if Saudi had the ability to pump up to 12.5 million bpd then why did it not produce this to the maximum degree at this point, given that the core aim of the 2014-2016 Oil Price War was to destroy the US shale sector, crashing prices by producing as much oil as possible? The answer was very simple: it was producing the most crude oil that it could, based on its true oil production figure of around 8 million bpd (therefore an extra 2.5 million bpd equaled 10.0-10.5 million bpd, the very figure it managed just about to achieve) and not on its nonsense figure of oil production of 10 million bpd (which another 2.0-2.5 million bpd would boost to 12.0-12.5 million bpd).

Finally, crude oil production. As highlighted in the two previous paragraphs from 1973 to the end of last week, Saudi Arabia pumped an average of 8.162 million barrels per day of crude oil. Not 10 million, 11 million, 12 million, 13 million, or any other ridiculous figure that it suits the Saudis to dream up: 8.162 million barrels per day, 8.162 million barrels per day, 8.162 million barrels per day. Why does the Kingdom lie about this? Simple: without its oil power the country has no real power at all, so enormously exaggerating its crude oil reserves, spare capacity, and production figures is geared towards puffing itself up in terms of geopolitical importance. In order to obfuscate these real numbers, the Saudis have devised the semantic trickery of interchangeably switching the use of the word ‘production’ with ‘capacity’ or even ‘supply to the market’. The two sets of words do not mean the same thing at all, and the Saudis know it.

How deep into the ground do we have to go to tap the resources we need to keep the lights on? How deep into the ground are we able to go?

The first oil well drilled in Texas in 1866 was a little over 100 feet deep: the No 1 Isaac C. Skillern struck oil at a depth that, from today’s perspective, is ridiculously shallow.

Ten years ago, data from the Energy Information Administration shows the average depth of U.S. exploration oil wells was almost 7,800 feet. It’s safe to assume that over these past 10 years, the average well depth has only increased.

The Bertha Rogers No 1 natural gas well in the Anadarko Basin used to be the deepest in the world, at over 31,400 feet. Unfortunately, at this depth the drillers struck liquid sulfur, which put an end to plans to continue drilling.

BP’s Tiber field in the Gulf of Mexico, drilled by the infamous Deepwater Horizon, became the location for the deepest oil well. The Tiber well’s depth was more than 35,000 feet.

There is also a record-breaker in terms of water depth: Maersk Drilling’s Raya-1 well offshore Uruguay was drilled in water depths of 3,400 meters or 11,156 feet.

2019-10-27 The Biggest Oil & Gas Discoveries Of 2019

Conventional oil and gas discoveries have fallen to their lowest in 70 years. All in all, this year has seen new discoveries of nearly 8 billion barrels of oil equivalent, compared to 10 billion barrels of oil equivalent discovered last year, so only one barrel out of every six consumed is being replaced with new resources.

Not only has the pace of discovery declined, but discoveries are also in much more challenging geological venues and typically offshore, which means it could take many years just to bring new resources online.

The age of discoveries onshore is over. The future game of discovery is decidedly in deep waters.

Earlier this month BP released its Statistical Review of World Energy 2019. The U.S. extended its lead as the world’s top oil producer to a record 15.3 million BPD (my comment: minus 4.3 million BPD natural gas liquids, which really shouldn’t be included since they aren’t transportation fuels). In addition, the U.S. led all countries in increasing production over the previous year, with a gain of 2.18 million BPD (equal to 98% of the total of global additions),… which helped offset declines from Venezuela (-582,000 BPD), Iran (-308,000 BPD), Mexico (-156,000 BPD), Angola (-143,000 BPD), and Norway (-119,000 BPD).

Peak demand? Hardly: “the world set a new oil production record of 94.7 million BPD, which is the ninth straight year global oil demand has increased.

After 20 charts showing global oil production Matt concludes “When US shale oil peaks and Iraq can no longer increase production there will be some surprises for a complacent world which should have used the 2008 oil price shock as a warning to get away from oil – voluntarily.”

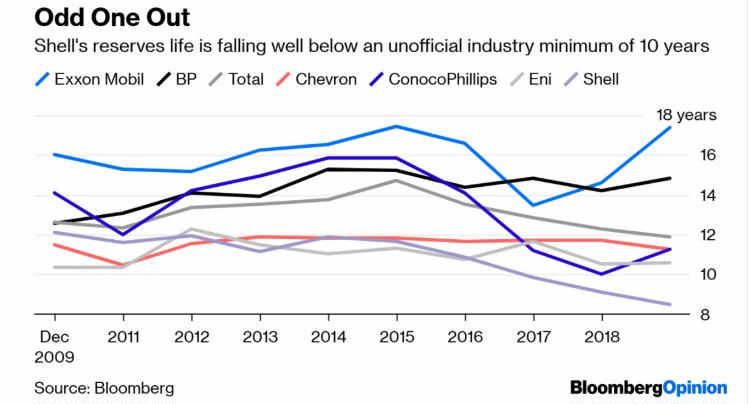

An oil company that doesn’t increase its reserves eventually runs out of product to sell, so having 10 years of reserve life is traditionally considered a bare minimum for oil supermajors (for our purposes, take these to be Shell plus Exxon Mobil Corp., BP Plc, Total SA, Chevron Corp., ConocoPhillips, and Eni SpA). Shell crossed below the 10-year level all the way back in 2016, and the figure at the end of 2018 stood at just 8.5 years.

Mexico’s existing oil reserves are dwindling so fast the country could go dry within nine years without new discoveries according to the National Hydrocarbons Commission, which said reserves fell 10.6% to 9.16 billion barrels in 2016, from 10.24 billion barrels a year earlier. Once the world’s third largest crude producer, Mexico’s proven reserves have declined 34% since 2013.

The decline in proven reserves is driven by record-low drilling activity the last three years. State-owned producer Petroleos Mexicanos drilled 21 wells last year, a record low, after averaging 31 per year since 2010.

Exxon Mobil Corp. may be facing “irreversible decline” as the oil giant fails to cope with low oil prices and mounting debt, a report released Wednesday found.The Texas-based company has suffered a 45% drop in revenue over the past 5 years as it bet big on drilling in oil sands, the Arctic and deep-sea sites ― decisions that proved expensive, environmentally risky and politically controversial.

Combined with a two-year plunge in oil prices, ballooning long-term debt to cover dividend payments to shareholders and an evaporating pool of cash, Exxon Mobil’s finances show “signs of significant deterioration,” according to new research from the Institute for Energy Economics and Financial Analysis, a nonprofit based in Cleveland.

“Investors right now are getting less cash from Exxon than they have historically, and are likely to get less cash in the future,” Tom Sanzillo, director of finance at the IEEFA, told The Huffington Post on Wednesday. “This is going to be a much smaller company in the future, and the oil industry is going to be much smaller in the future.”

In April, Exxon Mobil was stripped of Standard & Poor’s top credit rating for the first time since the 1930s. The rating agency said it worried Exxon took on billions in debt to fund new drilling projects at a time when oil prices were high. Now, with the price of crudebelow $50 per barrel, that debt looks risky. Despite S&P specifically citing such payments in its downgrade, Exxon Mobil actually increased its dividend by 2 cents the next day.

Usually, dividends go up as a company’s stock price thrives. But shares of Exxon have trailed the S&P 500 for 10 quarters in a row, the report noted, and that’s before factoring in the risks of climate change.

Dellanoy L et al (2021) Peak oil and the low-carbon energy transition: A net-energy perspective. Applied Energy 304.

EIA (2022) International Energy Statistics. Petroleum and other liquids. Data Options. U.S. Energy Information Administration. What’s important is THE Crude oil including lease condensate because this is the segment of petroleum that is a transportation fuel, many of the others are only good for plastics, heating and non-transportation uses. 2021 isn’t available yet, here are the years before that: 2018 83,053 2019 82,340 2020 76,101

Fustier K, Gray G, Gundersen C, et al (2016) Global oil supply. Will mature field declines drive the next supply crunch? HSBC global research.

Geiger J (2022) U.S. Shale Could Peak In 2024: Energy Aspects. oilprice.com

Source: Ben Adler. Aug 25, 2014. Europe is burning our forests for “renewable” energy. Wait, what? grist.org

Preface: By far the largest renewable energy resource used in Europe is wood. In its various forms, from sticks to pellets to sawdust, wood (or to use its fashionable name, biomass) accounts forhalf of Europe’s renewable-energy consumption.

Although Finland is the most heavily forested country in Europe, with 75% of their land covered in woods, they may not have enough biomass to replace coal when all coal plants are shut down by 2029. Much of their land has no roads or navigable waterways, so imports are cheaper than using their own forests (Karagiannopoulos 2019).

Vaclav Smil, in his 2013 book “Making the Modern World: Materials and Dematerialization” states: “Straw continues to be burned even in some affluent countries, most notably in Denmark where about 1.4 Mt of wheat straw (nearly a quarter of the total harvest) is used for house heating or even in centralized district heating and electricity generation.”

In the news:

2023: Enviva, the world’s largest biomass energy company, is near collapse. Enviva, is the world’s largest producer of wood pellets. They are burned in former coal power plants to make energy at an industrial scale. The company seems near collapse. Founded in 2004, Enviva harvests forests in the U.S. Southeast, with its 10 plants key providers of wood pellets to large power plants in the EU, U.K., Japan and South Korea — nations that use a scientifically suspect carbon accounting loophole to count the burning of forest wood as a renewable resource. A former manager and whistleblower at Enviva said that the company’s green claims were fraudulent. Last week, he said that much of Enviva’s downfall is due to cheaply built factories equipped with faulty machinery and large-scale fiscal miscalculations regarding wood-procurement costs.

2022 BBC UK power station owner cuts down primary forests in Canada. A company that has received billions of pounds in green energy subsidies from UK taxpayers is cutting down environmentally-important forests, a BBC Panorama investigation has found. Drax runs Britain’s biggest power station, which burns millions of tonnes of imported wood pellets – which is classed as renewable energy. The BBC has discovered some of the wood comes from primary forests in Canada. Ecologist Michelle Connolly told Panorama the company was destroying forests that had taken thousands of years to develop. “It’s really a shame that British taxpayers are funding this destruction with their money. Logging natural forests and converting them into pellets to be burned for electricity, that is absolutely insane,” she said.

Burning wood produces more greenhouse gases than burning coal. The electricity is classed as renewable because new trees are planted to replace the old ones and these new trees should recapture the carbon emitted by burning wood pellets. But recapturing the carbon takes decades and the off-setting can only work if the pellets are made with wood from sustainable sources. Primary forests, which have never been logged before and store vast quantities of carbon, are not considered a sustainable source. It is highly unlikely that replanted trees will ever hold as much carbon as the old forest.

Which source of renewable energy is most important to the European Union? Solar power, perhaps? (Europe has three-quarters of the world’s total installed capacity of solar photovoltaic energy.) Or wind? (Germany trebled its wind-power capacity in the past decade.) The answer is neither.

By far the largest so-called renewable fuel used in Europe is wood.

In its various forms, from sticks to pellets to sawdust, wood (or to use its fashionable name, biomass) accounts for about half of Europe’s renewable-energy consumption.

In some countries, such as Poland and Finland, wood meets more than 80% of renewable-energy demand. Even in Germany, home of the Energiewende (energy transformation) which has poured huge subsidies into wind and solar power, 38% of non-fossil fuel consumption comes from the stuff. After years in which European governments have boasted about their high-tech, low-carbon energy revolution, the main beneficiary seems to be the favored fuel of pre-industrial societies.

The idea that wood is low in carbon sounds bizarre. But the original argument for including it in the EU’s list of renewable-energy supplies was respectable. If wood used in a power station comes from properly managed forests, then the carbon that billows out of the chimney can be offset by the carbon that is captured and stored in newly planted trees. Wood can be carbon-neutral. Whether it actually turns out to be is a different matter. But once the decision had been taken to call it a renewable, its usage soared.

In the electricity sector, wood has various advantages. Planting fields of windmills is expensive but power stations can be adapted to burn a mixture of 90% coal and 10% wood (called co-firing) with little new investment. Unlike new solar or wind farms, power stations are already linked to the grid. Moreover, wood energy is not intermittent as is that produced from the sun and the wind: it does not require backup power at night, or on calm days. And because wood can be used in coal-fired power stations that might otherwise have been shut down under new environmental standards, it is extremely popular with power companies.

Money grows on trees

The upshot was that an alliance quickly formed to back public subsidies for biomass. It yoked together greens, who thought wood was carbon-neutral; utilities, which saw co-firing as a cheap way of saving their coal plants; and governments, which saw wood as the only way to meet their renewable-energy targets. The EU wants to get 20% of its energy from renewable sources by 2020; it would miss this target by a country mile if it relied on solar and wind alone.

The scramble to meet that 2020 target is creating a new sort of energy business. In the past, electricity from wood was a small-scale waste-recycling operation: Scandinavian pulp and paper mills would have a power station nearby which burned branches and sawdust. Later came co-firing, a marginal change. But in 2011 RWE, a large German utility, converted its Tilbury B power station in eastern England to run entirely on wood pellets (a common form of wood for burning industrially). It promptly caught fire.

Undeterred, Drax, also in Britain and one of Europe’s largest coal-fired power stations, said it would convert three of its six boilers to burn wood. When up and running in 2016 they will generate 12.5 terawatt hours of electricity a year. This energy will get a subsidy, called a renewable obligation certificate, worth £45 ($68) a megawatt hour (MWh), paid on top of the market price for electricity. At current prices, calculates Roland Vetter, the chief analyst at CF Partners, Europe’s largest carbon-trading firm, Drax could be getting £550m a year in subsidies for biomass after 2016—more than its 2012 pretax profit of £190m.

With incentives like these, European firms are scouring the Earth for wood. Europe consumed 13m tonnes of wood pellets in 2012, according to International Wood Markets Group, a Canadian company. On current trends, European demand will rise to 25m-30m a year by 2020.

Europe does not produce enough timber to meet that extra demand. So a hefty chunk of it will come from imports. Imports of wood pellets into the EU rose by 50% in 2010 alone and global trade in them (influenced by Chinese as well as EU demand) could rise five- or sixfold from 10m-12m tonnes a year to 60m tonnes by 2020, reckons the European Pellet Council. Much of that will come from a new wood-exporting business that is booming in western Canada and the American south. Gordon Murray, executive director of the Wood Pellet Association of Canada, calls it “an industry invented from nothing”.

Prices are going through the roof. Wood is not a commodity and there is no single price. But an index of wood-pellet prices published by Argus Biomass Markets rose from €116 ($152) a tonne in August 2010 to €129 a tonne at the end of 2012. Prices for hardwood from western Canada have risen by about 60% since the end of 2011.

This is putting pressure on companies that use wood as an input. About 20 large saw mills making particle board for the construction industry have closed in Europe during the past five years, says Petteri Pihlajamaki of Poyry, a Finnish consultancy (though the EU’s building bust is also to blame). Higher wood prices are hurting pulp and paper companies, which are in bad shape anyway: the production of paper and board in Europe remains almost 10% below its 2007 peak. In Britain, furniture-makers complain that competition from energy producers “will lead to the collapse of the mainstream British furniture-manufacturing base, unless the subsidies are significantly reduced or removed”.

But if subsidising biomass energy were an efficient way to cut carbon emissions, perhaps this collateral damage might be written off as an unfortunate consequence of a policy that was beneficial overall. So is it efficient? No.

Wood produces carbon twice over: once in the power station, once in the supply chain. The process of making pellets out of wood involves grinding it up, turning it into a dough and putting it under pressure. That, plus the shipping, requires energy and produces carbon: 200kg of CO2 for the amount of wood needed to provide 1MWh of electricity.

This decreases the amount of carbon saved by switching to wood, thus increasing the price of the savings. Given the subsidy of £45 per MWh, says Mr Vetter, it costs £225 to save one tonne of CO2 by switching from gas to wood. And that assumes the rest of the process (in the power station) is carbon neutral. It probably isn’t.

A fuel and your money

Over the past few years, scientists have concluded that the original idea—carbon in managed forests offsets carbon in power stations—was an oversimplification. In reality, carbon neutrality depends on the type of forest used, how fast the trees grow, whether you use woodchips or whole trees and so on. As another bit of the EU, the European Environment Agency, said in 2011, the assumption “that biomass combustion would be inherently carbon neutral…is not correct…as it ignores the fact that using land to produce plants for energy typically means that this land is not producing plants for other purposes, including carbon otherwise sequestered.

Tim Searchinger of Princeton University calculates that if whole trees are used to produce energy, as they sometimes are, they increase carbon emissions compared with coal (the dirtiest fuel) by 79% over 20 years and 49% over 40 years; there is no carbon reduction until 100 years have passed, when the replacement trees have grown up. But as Tom Brookes of the European Climate Foundation points out, “we’re trying to cut carbon now; not in 100 years’ time.

In short, the EU has created a subsidy which costs a packet, probably does not reduce carbon emissions, does not encourage new energy technologies—and is set to grow like a leylandii hedge.

The United Kingdom has announced plans to build the world’s largest biomass power plant. The Tees Renewable Energy Plant (REP) will be located in the Port of Teesside, Middlesbrough and it will have a capacity of 299 MW. While the plant is designed to be able to function on a wide range of biofuels, its main intended power sources are wood pellets and chips, of which the plant is expected to use more than 2.4 million tons a year. The feedstock will be sourced from certified sustainable forestry projects developed by the MGT team and partners in North and South America, and the Baltic States, and supplied to the project site by means of ships.

Wood pellets, which are low in sulphur and chlorine, will be primarily used to fuel the plant.

A biomass power plant of this type is referred to as a combined heat and power (or CHP) plant. It will generate enough renewable energy to supply its own operations and commercial and residential utility customers in the area.

Investment in the renewable project is estimated to reach £650m ($1 billion), which will be partly funded through aids from the European Commission, and construction works would create around 1,100 jobs. Environmental technology firm Abengoa, based in Spain, along with Japanese industry giant Toshiba will be leading the project for their client, MGT Teesside, subsidiary to the British utility MGT Power.

The feedstock will be burned to generate steam at 565°C that will drive a steam turbine, which will rotate the generator to produce electricity. The generated power will be conveyed to the National Grid.The exhaust steam generated by the steam turbine plant will be condensed by the ACCs and re-used, whereas the flue gases from the CFB boiler will be discharged via the exhaust stack.

Nitrogen dioxide (NO2) emissions will be minimized by using capture technology, fabric filters will reduce emission of particulate matter or dust and check the sulphur content of the fuel feed, while sulphur dioxide (SO2) emissions will be reduced through limestone injection into the boiler.

References

Karagiannopoulos, L. 2019. Finland Will Need to Import Biomass to Keep Warm. Reuters.

Preface. These are updates to Ward & Brownlee’s book “Rare Earth: Why Complex life is Uncommon in the Universe”. If we are one of the few planets with intelligent life, what a shame it would be if we destroyed ourselves and millions of other species in the 6th mass extinction we are causing, or nuclear winter, or continuing to exceed planetary boundaries. Maybe we aren’t so intelligent after all.

For combustion to occur, a planet needs an atmosphere of at least 18% oxygen. Less than that might allow complex multicellular life, but without a concentration of over 18%, there can be no fire, no combustion from diesel or gasoline engines, no steam turbines. So no technology, let alone propelling starships to other galaxies. You couldn’t even build them: it takes oxygen to generate high heat to extract metals from ores and make steel, copper, and other products such as glass, ceramics, bricks and more.

The article doesn’t go into this, but today that high heat is provided only by fossil fuels, yet another limiting factor for industrial technological civilizations – a planet would need both oxygen and fossil fuels. See the posts in this category for details: https://energyskeptic.com/category/fastcrash/industrial-heat/

A planet with oxygen of 30% and above would be a planet on fire since combustion would be too easy.

Perhaps thermal features could provide heat in a low-oxygen atmosphere, but such a civilization would have to remain very local, since geothermal heat isn’t transportable like wood, coal, and oil and impossible in a water world as well where the heat is coming from sea floor hydrothermal vents.

Scientists looking for life in the universe would be wise to look for planets with atmospheres containing 18 to 21% oxygen, the optimum level for useful combustion. Though today the telescopes viewing exoplanets can’t do that. And there is a chance of false positives where there is oxygen but no life exists, but Krissansen-Totton et al (2021) have found ways to rule them out (here).

If oxygen is the bottleneck that limits intelligent life, that might help solve the Fermi paradox which asks why there is no evidence of intelligent life given the size of the universe.

Sauterey B et al (2022) Early Mars habitability and global cooling by H2-based methanogens. Nature Astronomy https://doi.org/10.1038/s41550-022-01786-w

Re-creating Mars as it was four billion years ago using climate and terrain models, researchers concluded methane-producing microbes could once have thrived centimeters below much of the Red Planet’s surface, consuming hydrogen and CO2 while protected by the sediment above. But freezing temperatures of its own making may have driven them deeper, triggering global cooling that caused the surface to be covered in ice, killing them.

Koberlein B (2022) Venus’ atmosphere stops it from locking to the sun. universetoday.com

Of the thousands of exoplanets we’ve discovered, most of them closely orbit red dwarf stars. Part of this is because planets with short orbital periods are easier to find, but part of this is that red dwarf stars make up about 75% of the stars in our galaxy. Most are likely tidally locked, which means that only one side of the planet faces the sun which happens from tidal forces created by rotating around their sun so closely. But there may be exceptions. Earth rotates every 24 hours, Venus every 243 days. So instead of “fire and ice” tidally locked planets, these would be planets with hot, dense atmospheres (my comment: neither sounds friendly to life!)

Voosen (2022) The Planet Inside. Scientists are probing the secrets of the inner core and learning how it might have saved life on earth. Science 376: 18-22.

Earth’s inner core generates the protective magnetic field shielding our planet from damaging radiation. The magnetic field was sputtering to just 10% of what we have today 565 million years ago. Then miraculously, over just tens of millions of years, it regained its strength and not long after the multicellular life of the Cambrian explosion occurred with the birth of the inner core, a sphere of solid iron that spins independently from the rest of the planet. If this hadn’t happened Earth’s developing life in the ocean would have been exposed to far more radiation from solar flares, and rising oxygen levels would have escaped to space from the increased ionization.

Ziyi Zhu et al (2022) The temporal distribution of Earth’s super mountains and their potential link to the rise of atmospheric oxygen and biological evolution, Earth and Planetary Science Letters. DOI: 10.1016/j.epsl.2022.117391

Giant mountain ranges at least as high as the Himalayas and stretching up to 5,000 miles (8,000 km) across entire super-continents played a crucial role in the evolution of early life on Earth, which only formed twice in Earth’s history—the first between 2,000 and 1,800 million years ago and the second between 650 and 500 million years ago. Both mountain ranges rose during most important periods of evolution. The first range coincided with the appearance of eukaryotes, organisms that later gave rise to plants and animals. The second range coincided with the appearance of the first large animals 575 million years ago and the Cambrian explosion 45 million years later, when most animal groups appeared in the fossil record. When the mountains eroded they provided essential nutrients like phosphorous and iron to the oceans, supercharging biological cycles and driving evolution to greater complexity. The super-mountains may also have boosted oxygen levels in the atmosphere, needed for complex life to breathe. There is no evidence of other super-mountains forming at any stage between these two events, making them even more significant.

“The time interval between 1,800 and 800 million years ago is known as the Boring Billion, because there was little or no advance in evolution,” co-author Professor Ian Campbell said. “The slowing of evolution is attributed to the absence of super mountains during that period, reducing the supply of nutrients to the oceans.”

2021 Longer days on early Earth set stage for complex life. Extra light spurred oxygen release by mats of photosynthetic bacteria. Science 373: 607-608

Scientists have struggled to find a satisfying reason of what triggered oxygen buildup and why it took so long. It may be that the increasing length of a day as Earth’s spin slowed enabled more photosynthesis from bacterial mats, allowing oxygen to build up in ancient seas and diffuse into the atmosphere. 4.5 billion years ago the length of a day was only 6 hours long. But by 2.4 billion years ago the pull of the Moon had slowed the spin to 21 hour days, which is when the Great Oxygenation Event occurred, and then again a billion years later.

2021 Stars less than half as hot as our Sun can not sustain Earth-like biospheres: not enough energy to sustain photosynthesis

A new study of exoplanets — planets beyond our solar system — has revealed that none of them, despite previously thought to be habitable, may have the right Earth-like conditions needed to sustain life. The research evaluated the amount of energy these Earth-like planets received from their host star and if it was enough for living organisms to “efficiently produce nutrients and molecular oxygen” that are critical for complex life. So planets orbiting cooler stars known as red dwarfs that smoulder at roughly a third of the Sun’s temperature, don’t receive enough energy to even activate photosynthesis. Although the number of planets in our Milky Way galaxy is in the thousands, those with conditions similar to Earth and in the habitable zone are not very common, the study stated. A habitable zone means the region around a star where the temperature is just right for liquid water to exist on the planet’s surface. There is only one exoplanet Kepler-442b, a rocky planet with a mass twice that of the Earth 1,200 light-years away, comes close to receiving the radiation necessary to sustain a large biosphere. Covone G et al (2021) Efficiency of the oxygenic photosynthesis on Earth-like planets in the habitable zone. Monthly Notices of the Royal Astronomical Society.

O’Callaghan J (2021) Venus’s surface may always have been too hot for oceans. New Scientist.

If this is so, then the window of time for planets to become habitable is even narrower than astronomers had thought. Even earth was only able to condense water early in its history because the sun was 25% dimmer, seemingly solving the “faint young sun paradox” when Earth was thought to have been too cold to support liquid water. Had it formed today, our planet might well have been a “steam Earth” like Venus.

Oluseyi H (2021) Intelligent life probably exists on distant planets — even if we can’t make contact, astrophysicist says. Washington Post.

But just four in our galaxy: If only one in a hundred billion stars can support advanced life, that means that our own Milky Way galaxy — home to 400 billion stars — would have four likely candidates. Of course, the likelihood of intelligent life in the universe is much greater if you multiply by the 2 trillion galaxies beyond the Milky Way.

It also helps that Earth’s atmosphere is transparent to visible light. On most planets, atmospheres are thick, absorbing light before it reaches the surface — like on Venus. Or, like Mercury, they have no atmosphere at all. Earth maintains its thin atmosphere because it spins quickly and has a liquid iron core, conditions that lead to our strong and protective magnetic field. This magnetosphere, in the region above the ionosphere, shields all life on Earth, and its atmosphere, from damaging solar winds and the corrosive effects of solar radiation. That combination of planetary conditions is difficult to replicate.

At the low end of consensus estimates among astrophysicists, there may be only one or two planets hospitable to the evolution of technologically advanced civilizations in a typical galaxy of hundreds of billions of stars. But with 2 trillion galaxies in the observable universe, that adds up to a lot of possible intelligent, although distant, neighbors.

Unfortunately, we’re unlikely to ever make contact with life in other galaxies. Travel by spaceship to our closest intergalactic neighbor, the Canis Major Dwarf, would take almost 750,000,000 years with current technology. Even a radio signal, which moves at close to the speed of light, would take 25,000 years.

2021 Water is essential for life – not just the medium but active participant

Water is often seen as the background in which other chemicals like DNA and protein are dissolved, but of 6500 reactions, 40% made or destroyed a molecule of water. When E. coli divides to form 2 new cells, every water molecule it contains is either transformed or drives a chemical reaction 3.7 times on average. This may also be key to the origins of life, since water would have determined which chemicals survived — the ones that were soluble in water and able to react with it.